Meet Jasmine. Jasmine is a college student attending State

University. Like many college students, Jasmine has a

lot things she needs to buy: books, laundry baskets, food, and so on, and she can pay

for those things with two types of money: debit or credit. Debit is money that comes from a personal

bank account. Credit is money that is lent to you by your

bank. For example, let’s say Jasmine has been

using a credit card. Each time Jasmine uses the card to buy something,

say a $100 textbook, her bank is loaning her the money. While that sounds nice, be warned, the bank

isn’t giving Jasmine this money for free. They expect her to pay a certain amount of

money each month, called interest, if she doesn’t totally pay off her balance by the

due date.

As you can imagine, this can get very expensive

very quickly, especially when factoring in the high annual interest rates, or APRs, that

are charged by these companies. However, there is a solution to this rather

scary problem. As long as Jasmine always pays off her balance

in full by her monthly due date, she’ll never pay a cent of interest. Jasmine is shocked and thrilled, but still

isn’t quite sold on credit-cards. After all, with all their flaws, are they

really worth using? The short answer: as long as you avoid running

up a balance, definitely! So why is that? Well, “free money” for starters. Most credit cards offer their users rewards,

like cash back or airline miles, each time they make a purchase. For example, let’s say Jasmine’s credit

card comes with 2% cashback. That means if Jasmine spends $500 per month,

then at the end of the month she’ll automatically get $10 back, no questions asked. Then, if that wasn’t good enough, responsibly

using a credit card also allows Jasmine to build a great credit score.

This is a calculated number between 300 and

850 that summarizes your credit history, covering everything from your payment history to the

age of your accounts. While we’ll teach you more about your credit

score, including how to get and improve it, in our next video “Credit Scores and Reports

101”, just for now know that most credit cards actually require a credit score of at

least 600, plus at least $15,000 in annual income and a reasonable debt payment to income

ratio, generally below 36%. However, thankfully for Jasmine, who lacks

both credit history and a full-time job, she shouldn’t have a problem getting a student

credit card. In fact, the online application will take

all of five minutes. She’ll just have to be a full-time student

of at least 18 years of age, with either a small amount of income, like from a part-time

job, or a creditworthy co-signer. However, at this point we have to say, be

careful. Taking on a co-signer is no small matter. The account is still in your name, so any

credit mistakes are on you and your co-signer, plus your co-signer is even liable for any

of your missed payments.

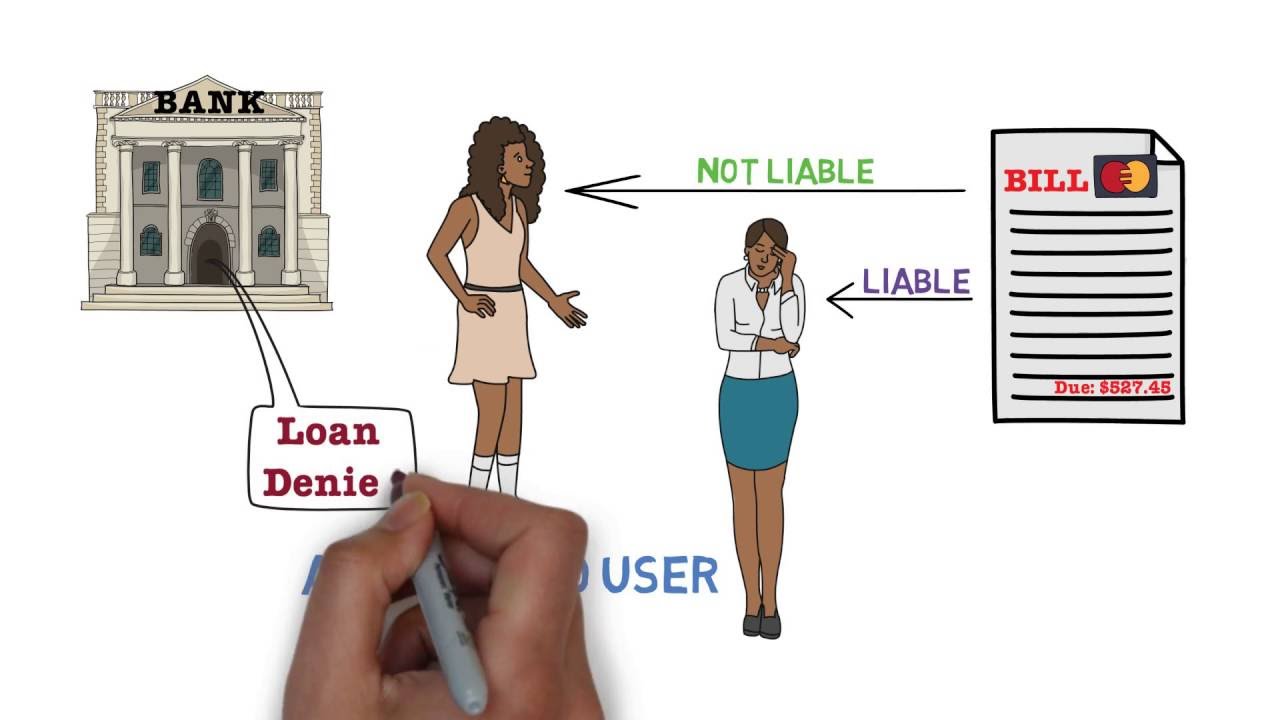

If Jasmine isn’t quite ready for that level

of responsibility, she can instead be added as an authorized user to her family’s account. Not only will this allow her to get her own

credit card, but in a few short months the credit bureaus will treat her parent’s credit

score as her own. Sounds pretty great right? Well, this strategy isn’t a cure-all.

Even though Jasmine isn’t liable for payments

on the account, her parents still are, plus many lenders will want to see you successfully

handling credit on your own before giving you a major loan. Hopefully you and Jasmine now understand the

basics of credit cards. Be sure to watch our next video, which covers

everything you need to know about credit scores, and be sure to check out our website, where

you can find more educational materials, your free credit score and great credit card recommendations..