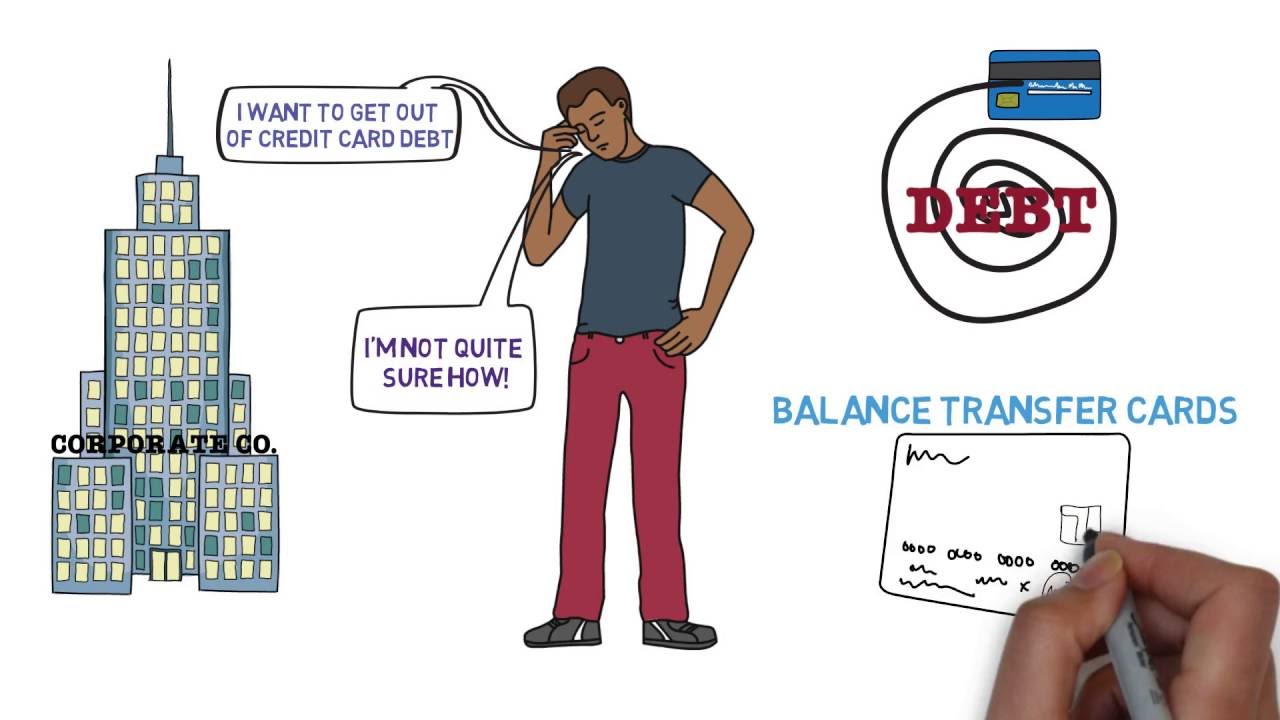

so let's say for example you have right now a $5,000 credit card okay that's the balance on this card you're paying 25% interest annually and that's about a $100 minimum payment every single month you're actually responsible for paying now all of a sudden by Magic you actually get an offer in the mail from a balance transfer credit card and you're like yo it must have been my luck it's not luck it's marketing your information has been sold thus the company knows about it and thus now they're sending you offers Direct offers to you now the offer says this we're going to give you 21 months to transfer your debt over to us and you get to pay it off in 21 months and we won't charge you any interest whatsoever for those first 21 months and you might say well this sounds like a great deal over here I'm paying for example a 100 bucks per month in interest but over here I'm going to be paying Z in interest for the first 21 months this saves me a bunch of money and the only catch is you have to pay a 3% fee for the entire balance transfer now that's not a big deal because right now you're paying $100 as a minimum payment and when you take 3% of 5,000 that's only about $150 or so so it's really not a big deal so why is this attractive what is the problem with it and what exactly is a balance transfer credit card I'm going to go into all the details in this video now do me a favor guys and ask you smash the like button I appreciate it a ton now the first thing is this guys okay a balance transfer credit card I'm not going to complicated it's basically just a credit card that is designed to actually get people that are in debt in some way to transfer their debt over to this credit card and potentially that company be the one that's actually going to get all that interest from you going further it's kind of like a long-term investment okay they're actually betting that you're not going to to pay it off in that introductory period and the TR going to keep the balance and you're going to continue to pay them and pay them and pay them and yes it could actually turn against them if you actually pay but for the most part they get 3% outright and if you don't pay them well you might become a customer for something else you might get another credit card with them or another product or a loan or a mortgage whatever it is okay they have a customer a prospect to get other things that is what a balance transfer is actually good for it now what is the problem here Tommy I still don't understand okay they're giving me an offer if I'm smart and I take advantage of it I walk away without paying any interest isn't that great well the answer is this okay you might think that you're actually going to walk away dilly dally free okay but what happens is usually this what's actually going on when you actually open up a Balan transfer credit card whether it's an offer whether you've been pre-approve approval whatever you just basically you basically just opened up another line of credit that is what's actually going on so let's say for example you have credit card a you owe $5,000 a year and now you actually get pre-approved for a balance for a credit card and then you basically apply and then say hey we're actually going to give you a balance of or a credit line of $7,000 and you say well that's awesome that's more than I had over here so now you say I want to transfer the balance from credit CR card a over to credit card B your new card the balance transer card and by the way it doesn't have to be a credit card it could also be for example Hospital loans it could be any debt overall even Collections and they could actually just basically pay that off by sending them a check and basically now you're in here and the debt is over here that's the whole idea okay so what happens is this okay you say I want to transfer balance from this card over to here they say okay just pay us a 3% fee you pay the 3% fee that's $150 they sent over a check to your credit card okay now that's fully paid off the balance on credit card a is basically zero the balance on your new balance crit card is basically um $5,000 or whatever the balance here basically was that's the idea now what actually happened here okay you went from having a credit line of $5,000 to having a credit line of basically $122,000 remember so if you got in value so far I'm going to ask for a favor subscribe to the channel because only like 20% of the people that watch or actually subscrib so go ahead and subscribe right now cuz I have a lot more content and having a credit line of basically $112,000 remember they actually gave you $7,000 and you have 21 months to pay that off okay without any interest and you might think this is awesome okay what I'm going to do is basically pay this off and never look back but what usually happens is this and I'm sad to say this okay but what usually happens is this okay you have credit card a now which is basically empty and you have credit card B all right and what happens is basically you say well this one is free you start using it again okay and before you know it this goes right back up to 5,000 or 3,000 or 4,000 and this one you're barely making any real payments or any Dent to it remember they gave you 5,000 the balance transfer credit card is still a credit card you can still use it to buy stuff and it still gave you $2,000 extra dollars and you actually need it so now you might use that for some things else okay and before you know it the 21 months have gone by and now you owe over $110,000 overall you owe credit card a you also go owe credit card B credit card B is saying yep we got them now we're actually collecting interest payments every single month from you and credit card a is saying well he paid it off but now he's back to pay now so I guess we win also so what is the right way to go about this and Tommy how have you ever done this the answer is I owed about wait for it $133,000 in credit card debt and I actually used balance transfer credit cards to actually help me clear all the debt now I was not one of the people that actually went ahead and basically clear credit card a transfer to credit card B and then build up a balance back in credit card a what I did was this I follow this three step system okay the first step is you want to set for yourself some really real istic goals based on how long they're actually going to give you interest free so overall let's say I actually owe $5,000 right that's how much I actually owe I'm going to divide this number by how many months you're actually going to give me so divided by 21 in this in this case by the way what credit card am I actually talking about I'm actually talking about the city Simplicity balance transfer credit card that offer 21 months to pay interest free 0% APR and even 12 12 months to actually buy things and not get charged any interest obviously they're doing this for a reason you transfer the balance over you get 21 months to pay it off but you also get 12 months to buy other crap and actually build up even a bigger balance don't be stupid don't fall for that okay so now I know that per month I need to pay about $240 to be debt free in21 months okay that's the idea and that's how I would actually do it now for me personally I would say well if if this is actually very doable I would stick to it if it's actually a little bit less than I can basically do I would actually lower it and basically even if I end with the balance okay at least I was actually realistic okay now for me personally I actually paid more towards it to be able to pay it off a lot faster I actually paid off $133,000 in credit card debt in 12 months okay because I actually fell for that trap where discover sent me a credit card and they were like Hey we're going to give you I think 18 months of purchase free interest and I went crazy okay I went crazy and what happened is I maxed out everything then it was like um I think it was 18 months right so I spent like 6 months doing some crazy stuff and then I had 12 months and I was like yo I need to pay all this in 12 months and I basically was able to cover everything in 12 months I think at a point I to transfer balance over to the balance transer card but I was actually able to do it which actually saved me a ton of money but it was only because I was smart so step number two is basically once you transfer the balance well close credit card a all right close it because you don't want to be at risk at rebuilding this actual um credit line and to actually get into double the debt you actually want to clear that and then lastly all right the balance CH credit card don't use it to get into more debt only use it to actually pay off the debt fast and be done with it and once you're done with all the debt my advice would be a 100% just close to to credit cards overall and don't get back into those problems okay ever since I became debt free and I don't have any credit cards I have no method no way of getting into debt anymore so it's not something I worry about but as long as you have that possibility that availability to watch you say I'm going to use this credit card for this or that for this emergency or that emergency you're always going to be going back into debt and going right back into where you landed I think the Bible says a dog is always going to return to his vomit and that's just disgusting okay so if debt is actually getting you into trouble over and over again and you're going back to it well that's just stupid and nonsense okay you actually want to avoid that so yes okay understand what they're trying to do they're trying to get you to bring your balance over to hopefully spend more money to be trapped with them and to pay them a bunch of interest but if you're smart what you're actually going to do is say I'm going to use you and I'm going to take advantage fully I'm going to close credit card a and once I'm done with you I'm also going to close you and I'm going to be done with it so set for yourself achievable goals so you're actually able to do this as fast as possible guys thanks for watching as always like subscribe hit the Bell sh notified there are obviously other balance of credit cards out there so if you know a few of them comment them down below if you want a full video on the offers out there let me know and I'll actually get to work up here is another video and this video is actually made possible by the supporters over at patreon here is a list of their names I appreciate it a ton if you actually want to join us on patreon support the channel the link is going to be down below thanks for watching as always like subscribe hit the Bell so you get notified peace