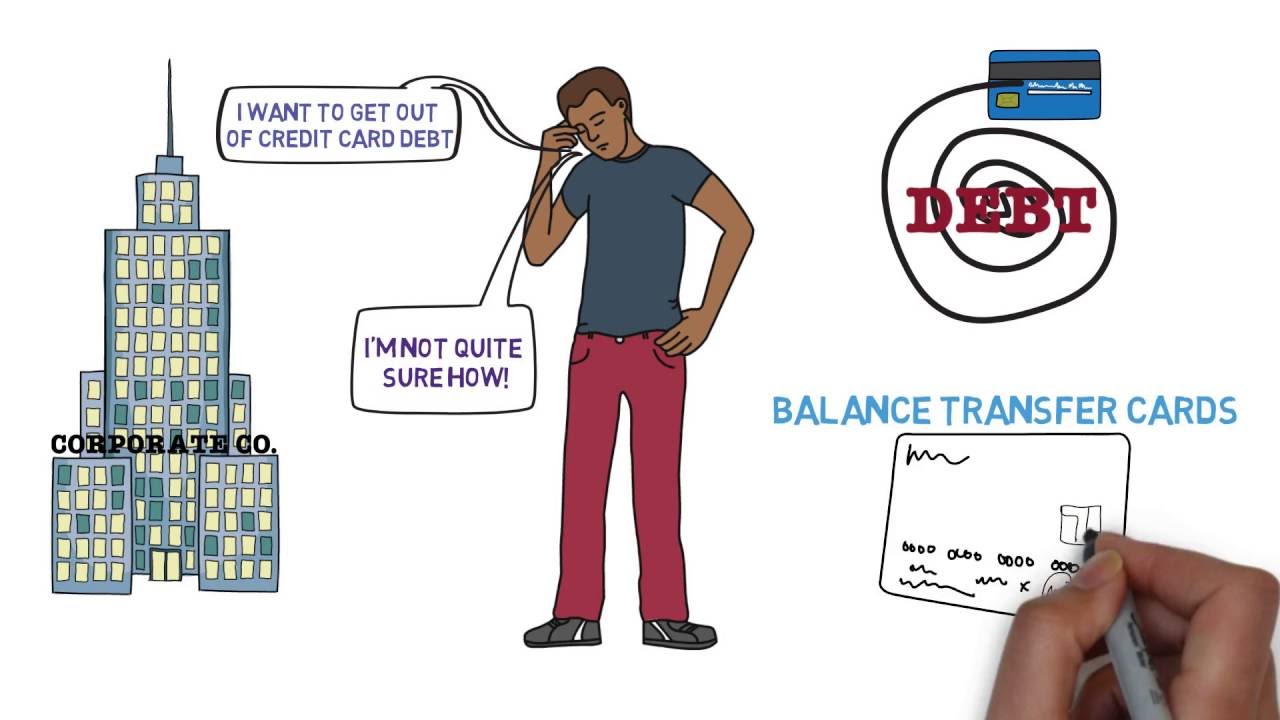

Meet Tom. Tom is a few years out college with a great

job and a lot credit card debt. Tom wants to get out of debt, but isn’t

quite sure how. Luckily for Tom, there exists a great solution

to his problem: balance transfer cards. However, before we continue, if Tom doesn’t

have a firm understanding of what a credit card or credit score is, or how to effectively

use either, we highly recommend watching our three videos “Credit Cards 101,” “Credit

Scores and Reports 101,” and “Credit Cards: Mistakes and Best Practices” before continuing

further. But let’s get back to the matter at hand. What is a balance transfer? Well, a balance transfer is simply the act

of transferring an existing credit balance to another credit card.

Most credit cards aren’t good this for:

they’ll immediately start charging interest on the transferred balance, plus a fee, generally

about 3-5% of the transferred balance. However, there is a specific subset of credit

cards, called balance transfer cards, that won’t immediately start charging interest,

instead giving Tom a 15-21 month window of 0% APR to pay off his balance interest-free. This is a great deal, but let’s still walk

through the steps you’ll need to take to get one: Step 1: Before doing anything, make a debt

repayment plan, ideally using our free recommended website, and rank your credit cards by interest

rate, as no matter what you end up doing, you’ll always want to tackle the highest

interest rate debt first.

Step 2: Once that’s done, call your credit

card company and try to get them to lower your APR. Emphasize that if they don’t agree, you’ll

move your balance to another company offering lower rates. Step 3: If the call fails and you still want

to transfer, keep in four three things. One: You’ll need good credit to get a balance

card. Two: You can’t transfer a balance to a card

offered by your current bank. Three: Depending of the size of your debt,

you may not be able to pay it off by the end of the promotional period, so have a plan

for that. And Four: The credit line on your balance

transfer card may be below your total debt load, meaning you’ll either have to:

Apply for a second balance transfer card Keep the remaining debt on your current card

and pay the high rate. Or use a personal loan, which is slightly

more expensive than a balance transfer card, but comes with a lower credit score requirement. And don’t worry, we’ll cover this option

in our next video. However let’s assume for now that Tom has

been approved for a balance transfer card with a high enough credit limit.

This is an important first step, but they’re

still a few more things to keep in mind: One: Don’t spend on the card, as the 0%

APR period may not extend to purchases. Two: Complete the transfer as fast as possible

or the 0% APR offer may expire. Three: Be careful about consolidate multiple

balances onto one card, as that will lower your credit score.

Four and Finally: Once you’ve completed

the transfer, always pay on time and don’t close out your old accounts, as failing to

follow either will lower your credit score. Hopefully you and Tom now better understand

balance transfer cards. Be sure to check out our next video, where

we’ll teach you how to get out of credit card debt without them, and be sure to website,

where you can find more educational content, your free credit score, and great credit card

recommendations..