Meet Tom. Tom is a few years out college with a great

job and a lot of credit card debt. He wants to get out of debt, but isn’t quite

sure how, especially because he didn’t qualify for a good enough balance transfer card, detailed

in our two-part video series “How to Get Out of Credit Card Debt”. While Tom may think all hope is lost, there

is another way: personal loans.

However, before we continue, if Tom doesn’t

have a firm understanding of what a loan is, or how to effectively use one, we highly recommended

watching our two videos “Loans 101” and “Loans: Mistakes and Best Practices” before

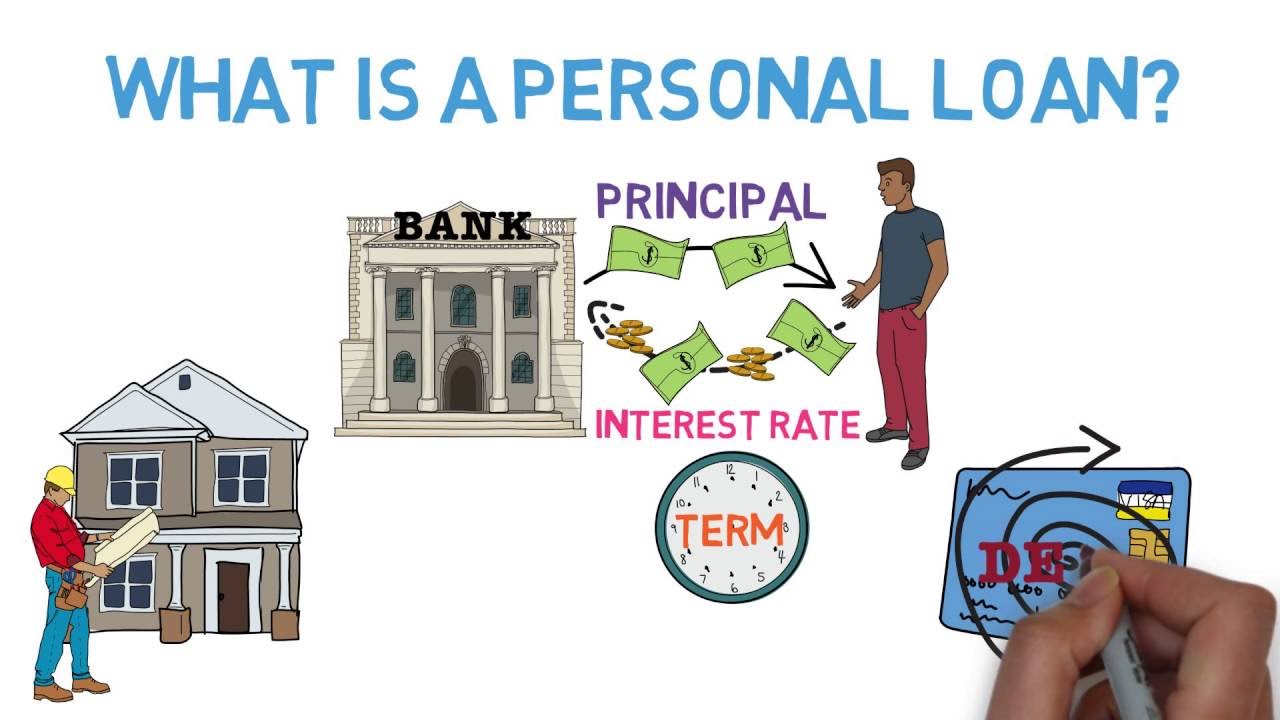

continuing further. But let’s get back to the matter at hand. What is a personal loan? Well, like most loans, personal loans offer

Tom a fixed amount of money at a certain interest rate for a set period of time. However, unlike most loans, personal loans

can be used for a wide variety of expenses, ranging from home improvement projects to

paying off credit card debt.

Speaking of credit cards, personal loans,

especially those from online lenders, will have interest rates lower than almost every

credit card. In addition, if Tom borrows from an online

lender that considers not just his credit score, of which he’ll need at least a 640,

but also his education status and earnings potential, those interest rates can be even

lower. Plus, even better, applying for a personal

loan from an online lender couldn’t be easier. All Tom needs to do is fill out a short credit

application. Then, the lender will likely use a “soft

pull” for his credit history, which won’t hurt his credit score, and within a few minutes,

Tony will be able to see the amount see can borrow and the APR he qualifies for, a process

he can then repeat at multiple online lenders. Should Tom instead choose to get personal

loan from an offline lender, like a big bank or credit union, which just have one warning.

These institutions tend to have higher interest

rates due to their much greater overhead, plus they tend to avoid “soft-pulls”,

which makes it harder to check your rates without hurting your credit score. So let’s assume Tom has chosen to get a

personal loan through an online lender. What’s his next step? Well, assuming he’s chosen his lender and

has checked his rates, he can then fill out the actual loan application online.

This should be very simple process, but there

is one thing to watch out for. Online lenders often charge a nonrefundable

origination fee for creating the loan, generally ranging between 1-5% of the loan’s value. This generally means two things:

One: If Tom wants to borrow exactly $10,000, and has to pay a 1% origination fee he’ll

need to borrow $10,100 dollars instead. Two: If Tom wants to use the loan proceeds

to pay off credit card debt, he needs to make sure the origination fee is less than the

interest he’ll save by using a personal loan. And don’t worry, our online calculator makes

this process a breeze. Finally, assuming the math checks out, Tom

just needs submits his application.

At this point, there will be a hard credit

check, but assuming Tom is approved, his bank account will generally be funded within a

few days. Tom is now on his way to being debt free. Congratulations! You’ve finished our personal loan basics

curriculum! If you want to see our free recommendations

for personal loan lenders, or just check out more educational material, be sure to check

out our website!.