How can I handle my creditors if I know I

cannot pay my bills? This is a question that comes up all the time. Now first, let me assure

you, there are many factors that can just reek havoc on your ability to pay your bills,

so you can have layoffs, maybe health or medical issues, maybe some other unexpected crosses.

Those types of situations will definitely and certainly affect your ability to repay,

so don't feel like you are alone, and don't feel like you're the first person that has

to speak with your creditors because you're going through such a crossly situation.

Call

your creditors, let them know that you cannot pay your bills at this point and time, but

also be sure to let them know the reason you cannot pay, and what it is you're going to

do about it. In other words, let them know what you can pay, and when they can expect

to receive payment, and then follow through, it is not appropriate for you to tell your

creditors one thing, and then do something else, they're counting on you to follow through

with what you tell them you would do.

Now if you tell them you can pay a certain amount,

it may be that they're even acceptable to having you pay that amount on an ongoing basis,

if so, you may want to pursue that and make it part of an extension of the loan or debt

that you currently have. Most importantly, you want to be sure and keep your utilities,

and any secured debt, such as your home, your automobiles, or something that you have an

asset setup against. You want to be sure that you keep the payments current on those items.

So far as medical bills, personal loans, or credit cards, those would be the ones that

you first want to negotiate. However, if you find that your home loan, which is usually

your largest loan, if you find that that's going to be unmanageable for you to make your

payments, you need to call them first, call your creditors and let them know what's going

on, and what you plan to do with it.

You want to know how to use your credit card

to save you some money. Well, sometimes you can save money by transferring the balances

of a higher interest rate credit card to a credit card that has a lower rate of interest.

And also, if you have problems making payments, then you may find that one card can incorporate

all your small credit card balances together into one payment each month. And then that

way you would have only that one payment to be concerned with. So you can use your credit

card to save money if you look at it from both of those perspectives..

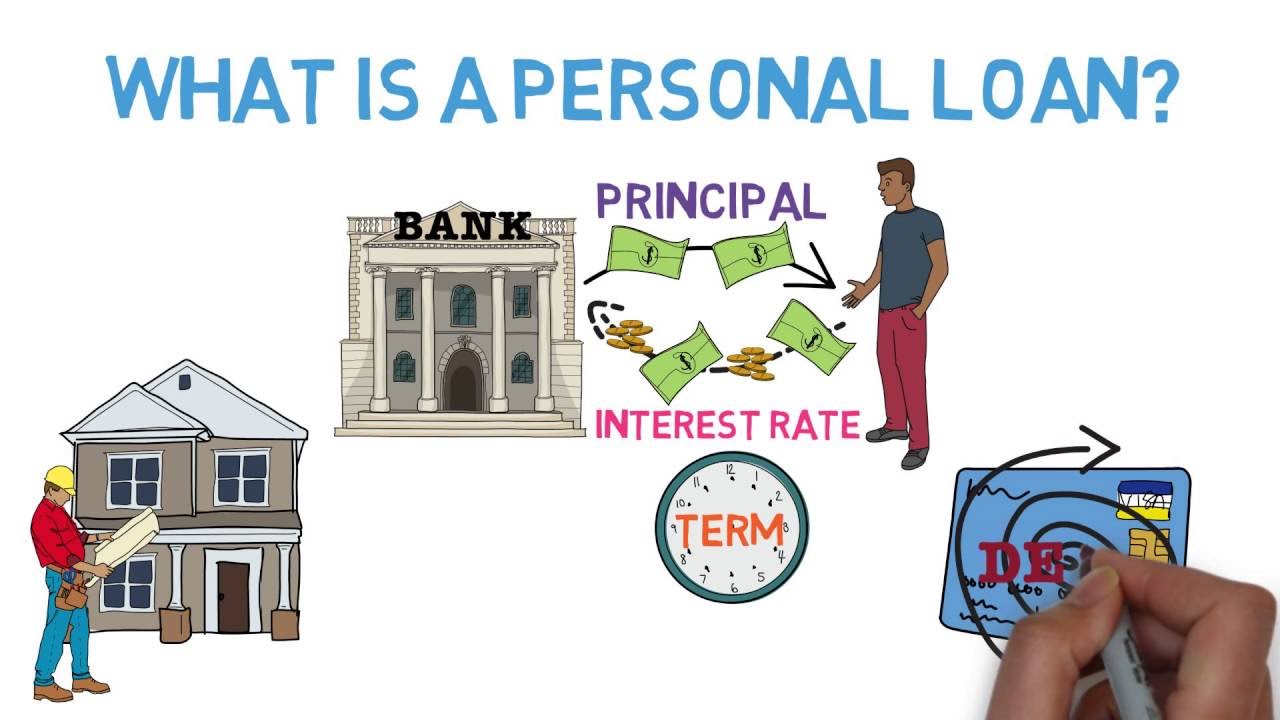

Meet Tom. Tom is a few years out college with a great

job and a lot of credit card debt. He wants to get out of debt, but isn’t quite

sure how, especially because he didn’t qualify for a good enough balance transfer card, detailed

in our two-part video series “How to Get Out of Credit Card Debt”. While Tom may think all hope is lost, there

is another way: personal loans.

However, before we continue, if Tom doesn’t

have a firm understanding of what a loan is, or how to effectively use one, we highly recommended

watching our two videos “Loans 101” and “Loans: Mistakes and Best Practices” before

continuing further. But let’s get back to the matter at hand. What is a personal loan? Well, like most loans, personal loans offer

Tom a fixed amount of money at a certain interest rate for a set period of time. However, unlike most loans, personal loans

can be used for a wide variety of expenses, ranging from home improvement projects to

paying off credit card debt.

Speaking of credit cards, personal loans,

especially those from online lenders, will have interest rates lower than almost every

credit card. In addition, if Tom borrows from an online

lender that considers not just his credit score, of which he’ll need at least a 640,

but also his education status and earnings potential, those interest rates can be even

lower. Plus, even better, applying for a personal

loan from an online lender couldn’t be easier. All Tom needs to do is fill out a short credit

application. Then, the lender will likely use a “soft

pull” for his credit history, which won’t hurt his credit score, and within a few minutes,

Tony will be able to see the amount see can borrow and the APR he qualifies for, a process

he can then repeat at multiple online lenders. Should Tom instead choose to get personal

loan from an offline lender, like a big bank or credit union, which just have one warning.

These institutions tend to have higher interest

rates due to their much greater overhead, plus they tend to avoid “soft-pulls”,

which makes it harder to check your rates without hurting your credit score. So let’s assume Tom has chosen to get a

personal loan through an online lender. What’s his next step? Well, assuming he’s chosen his lender and

has checked his rates, he can then fill out the actual loan application online.

This should be very simple process, but there

is one thing to watch out for. Online lenders often charge a nonrefundable

origination fee for creating the loan, generally ranging between 1-5% of the loan’s value. This generally means two things:

One: If Tom wants to borrow exactly $10,000, and has to pay a 1% origination fee he’ll

need to borrow $10,100 dollars instead. Two: If Tom wants to use the loan proceeds

to pay off credit card debt, he needs to make sure the origination fee is less than the

interest he’ll save by using a personal loan. And don’t worry, our online calculator makes

this process a breeze. Finally, assuming the math checks out, Tom

just needs submits his application.

At this point, there will be a hard credit

check, but assuming Tom is approved, his bank account will generally be funded within a

few days. Tom is now on his way to being debt free. Congratulations! You’ve finished our personal loan basics

curriculum! If you want to see our free recommendations

for personal loan lenders, or just check out more educational material, be sure to check

out our website!.

Wow! What a house! Maybe a little much for me, though. Okay, this is probably more like what I can afford. Unless, I could borrow the money to get something a little bigger. Perfect. But, borrowing means that I could be in debt. And for a lot of people, that can be intimidating. But debt is really just a way of borrowing money, with the promise of paying it back with interest. That sounds okay, right? Unless. I would take out a big loan that I couldn't pay back. People take out loans all the time to buy houses, cars, to pay for school. All sorts of things. And it's not just people. Companies also borrow. And governments do it too. When a government borrows, it's called public debt or sovereign debt. Governments raise this money by issuing bonds, and then selling them to the public with a guarantee that they'll pay them back. Just like people, countries need money to buy or build stuff that their income, mostly tax revenues, won't entirely pay for. Governments should invest their money wisely in things that help their citizens. Think of education or health care.

Governments can also invest in things that will generate revenue or grow the economy, like infrastructure projects. Governments can also use the money to reduce taxes or they can even give it directly to its citizens who need support. So why are economists sometimes concerned by public debt? Well, for all the benefits that these funds can bring, there are also risks. Let's take two countries to demonstrate. Here’s country A, and here’s country B. Now, let's say both of them have borrowed roughly the same amount of money at roughly the same time.

But looking closer, we can see they have very different economies, notably in size measured by gross domestic product, or GDP. Let’s look at their debt levels again, but this time as a percentage of their GDP. And, wow. You see the difference? Same debt, but very different outcomes. Countries are able to manage their debt when they borrow a reasonable amount relative to their ability to pay it. Country A’s economy is big enough to pay the interest on the debt. If Country B cannot pay things back, well, it gets harder to convince investors to lend you more money. And that is scary because it only gets harder from there. If an economic crisis hits, one of these guys will have the funds they need to respond. The other is going to need some help. The trick here is for governments like Country B to invest the money they borrow wisely, which can help keep debt manageable. So where does that leave me and my new house? Well, first, I need to adjust my own budget. I don't need that. That. That. You're gone. Definitely gone. And second, debt isn’t about living beyond my means.

It's about borrowing a reasonable amount relative to my ability to pay it. Even if I do splurge every now and again..

Growing up, you learned how to do things right. You went to school, got good grades, and now

you've started working. The paychecks are coming and you are happy

to receive them. You may have worked for 3, 5, or even 10 years

but your finances are not looking as good as your career. You are probably one or two paychecks away

from going broke. You know this is a problem, but you don’t

know how to fix it. Have you ever wondered why you have been so

successful in your career, but you seem to be struggling with your finances? The reason is simple.

Personal finance management is not taught

in schools, and it isn't taught at home either. Your school teachers were more concerned about

doing their jobs and grading your papers. Except in a few cases, your parents on their

part encouraged you to be a good student and also to become a responsible citizen. The reason both parties never talked to you

about financial management is that they didn't know it. Probably, they were also struggling with their

finances and never had solutions to their money problems. Managing your personal finance can be a tricky

task especially in the world that we are living in. If care is not taken, even the most prudent

person could slip and find themselves in a financial mess. Do you know why? It is easy to spend the money you earn.

Your bank accounts are linked to multiple

services. Placing an order or making a purchase could

be as easy as a few clicks on your computer or mobile phone. If you want to make the most from the money

that you earn, you must plan for it. You must live in constant awareness of the

money that is coming in and how it is going out. Without the right information, you may not

know how to come out of the rat race most people have found themselves in. That is why we are looking at how you can

be in total control of the money you earn and the things you are spending your money

on. You can effectively account for your money

only if you manage your finances properly. Are you getting some value from this video

so far? If you are, I would like you to do something

right now.

Pause the video. Go ahead and hit the ‘like’ button and

also click subscribe if you are new, and welcome. That way you will be notified of all our inspirational

videos any time we upload them. Done? Great! Let’s dive in. What is personal financial management? As a term, personal finance covers all aspects

of managing your money as well as saving and investing. This includes budgeting, investments, banking,

insurance, tax, mortgages, and retirement plans. Personal finance has to do with meeting your

personal financial goals including short-term, mid-term, and long-term goals. Personal financial management has to do with

your ability to know where you are financially at the moment and what you can do to make

the most out of your income in order to plan for a better future. This involves gaining control over your present

financial situation so that you can organize your daily expenses to match your plans and

expectations for the future.

The reasons why money management is important

1. Saving money

The questions you need to answer are these: What if you lose your paying job today? How far can you go before you get another

job? Have you ever heard the expression "Saving

for the rainy day"? It is important to have some money kept aside

that could save you from emergencies. 2. Security for your family

As you grow in life, your responsibilities will grow to catch up with you. You want to plan for your child’s college

education. You want to plan for your family's health

through insurance and other solutions. Planning for your family security is an essential

part of money management. 3. Investment opportunities

No matter how much you earn today, your needs will increase over time. Managing your money effectively will prepare

you for investment opportunities. You will learn how to pick the right kind

of investments. Having the right kinds of investments will

help you meet your growing needs in the future. Without proper management, you may not have

enough to meet your present needs. And if you can’t meet your present needs,

how are you going to have extra money to invest for your future needs? 4.

Better Living Standard

Are you happy with your present living standard? I’m sure you would like yourself and your

loved ones to enjoy a better living standard in the future. You want to own your own home, or at least

a better one. You want to go on vacation with your loved

ones to distant places. All this can only be accomplished if the money

you earn today is properly managed. 5. Increase in Financial Intelligence

The good thing about financial planning is that it exposes you to higher financial knowledge. When you start saving and making plans for

the future, you will need the services of financial advisors. As you plan and work closely with these experts,

your financial intelligence will increase. Make sure you build a relationship with financial

advisors that you can trust. Trusted advisors will be transparent and willing

to share their knowledge with you.

Over time, you may find that you are beginning

to take investment decisions on your own. Now that you have seen the reasons why you

must manage your finances, you also need to learn the strategies that you can apply to

get it right. Strategies to effectively manage your money

1. Budgeting

It is easy to spend most of your money on irrelevant purchases if you don't have a budget. Making unnecessary purchases will affect your

savings and leave you disappointed at the end of each month. You can get it right by making a proper budget. Map out different areas you want to allocate

your money. As you allocate money for your daily expenses,

also allocate money for your long-term goals such as investments. There are no rules of the thumb here. You should identify a budgeting plan that

is most suitable for you. Several budgeting apps have been created for

smartphone users. You can as well use excel sheets. Do a little research and identify the ones

that suit your purpose the most. A school of thought suggested a budgeting

method known as 50/30/20. A breakdown of this method goes like this:

Assign 50% of your income after taxes to essential living expenses such as rent, groceries, utilities,

and transport.

Assign 30% to casual expenses such as wear,

vacation, recreation, and charity (if you like). Assign 20% to future plans such as savings,

investment, and retirement plans. It doesn't matter how much you have had things

messed up. It is never too late to start. You can start today by drawing a budget for

yourself. 2. The right bank accounts

Operating the right bank accounts is necessary to successfully manage your finances.

You can set up checking, saving, and investment

accounts. These accounts will become the pillars of

your financial success. Your checking account should hold the money

you use for your regular purchases. You should not leave your savings in a checking

account. Keep your savings in a separate account designed

for that purpose. If not, you could constantly interfere with

your savings and squander it on unplanned purchases. Also, fund your investment accounts and be

consistent with them. 3. Emergency fund

One thing about life is that unexpected expenses show up from time to time. What happens if you weren’t prepared for

it? No one prays for misfortune but as long as

we live on planet Earth, situations beyond our control will surface. Set money aside for unexpected situations

such as the loss of a job. You should save up money in your emergency

fund that should last you up to 6 months assuming you lost your job.

Your emergency fund should also hold funds

for situations such as medical bills, major house repairs, or a huge car repair. 4. Keep track of your finances daily

You must check in with your finances daily. This shouldn't take much of your time. Dedicate 5-10 minutes of your time to it daily

and you will be good. Keep track of all your purchases and keep

receipts. Enter your spending into an excel sheet or

the budgeting app you are using. That way, you will know when you start spending

above your budget. 5. Clear up debts

Debt could be a major hindrance when you start working to achieve your financial goals. Identify the recurrent debts that you have

and start with the biggest ones. If you have many accumulated debts, then you

may have to set up a debt repayment plan. Allocate a good chunk of your income to paying

up these debts and aim at clearing them as soon as possible. You can take it up one after the other. Start with the biggest ones, and then the

next, until you have them all cleaned up. When you are done paying off your outstanding

debts, avoid getting into new debts.

Here are some tips that could help you clear

up your debts faster. • Set up a side hustle – If your current

income cannot pay off your debts quickly, you may consider starting a side hustle. A side hustle will not only bring in extra

cash that you need at the moment, but it will also position you to reach your future financial

goals faster. You can go online and research available work-from-home

jobs that you can do in your spare time. You can start with freelance jobs, drop shipping,

or affiliate marketing. Who knows, your side hustle could grow to

become a major source of income for you. • Get a second job – A second job will

be handy to help you clear up your debts. This may require some sacrifices on your part,

but you have to do whatever it will take to come out of debt and become financially free. • Sell off idle items in your home – If

you look around your home, you could find unused or unwanted items lying idle. Put them up for sale on online marketplaces

such as eBay. There could be someone out there searching

for that exact item and willing to pay for it.

• Cut down your budget in some places – Go

back to your budget. Look through your listed items. You may find some things you can do without. Take them off from the list or at least cut

down your budget for them. That way, you could find extra cash to pay

your debts faster. 6. Be smart with your credit cards

Credit cards have become an essential part of our financial activities. It seems unrealistic to not own one these

days. Credit cards provide convenience to us in

paying for goods and services, but they can also become major traps for debts.

Make sure you pay off your full balance every

month. If you can’t do that, then keep your credit

utilization ratio at a minimum. It means that you must strive to keep your

account balances below 30% of your total available credit. 7. Examine your credit score

Keep an eye on your credit card score. Your credit score is a three-digit number,

but it can make a great difference in your finances. If your credit card score is high, you will

attract lower interest rates and better loan terms from lending institutions. A good credit card score will become useful

when you apply for large loans such as a mortgage. Getting a low interest rate on a mortgage

could save you thousands of dollars. Here are some ways you can improve your credit

card score.

1. Get your credit report and check for errors. 2. Use a credit monitoring service to prevent

future errors. 3. Pay bills on time and keep your credit utilization

rate low. Late payment of bills is one of the fastest

ways to ruin your credit score. Well, that’s all for the video. If you are interested in more interesting

content. Check out these two videos. How businesses manage money Cashflow explained It’s Not About How Much You Make, It’s

About How Much You Keep Fundamental’s of Money Management Thank you guys so much for watching, have

a great day and I’ll see you all in the next one.

How do I live within my means and get out

of debt? Hmm, that's a question I'm often asked. And I'll tell you, while shopping seems

to have become the number one national pastime, you can, with just a few simple changes in

your every day routine, get out of debt and live within your means. First off, you have

to determine what you owe and estimate some type of budget. Now, you have to understand

that the budget's going to change over time, and as you realize that there's some things

maybe you didn't include or things that you've overestimated in it. You need to be responsible.

Do not underestimate your debts or your bills. And you need to get help from a consumer credit

counseling agency if you find that budgeting is just something that you're not able to

do. Then, next, you need to discuss at one time altogether with your entire family, your

entire household, about the budget needs. You have to be honest. Let them know where

you're at and what you're going to have to be doing.

It's not necessarily all about cutting

different expenses; it's about reaching goals so that you can live a happier, better life.

And don't play the blame game. You're not looking for any type of retribution to anyone

who has, perhaps, caused some past budget problems. You're looking to go forward to

create a truly workable budget that fits everyone in your family. Then you need to take feedback

from each other, from each family member, and you need to brainstorm about ideas of

how to cut expenses in certain areas and just embrace that there's a difference between

your wants and your needs.

You need to develop your goals and figure out methods of accountability.

You need to set a reasonable budget that incorporates everyone, and that it's a budget everyone

can follow. You need to realize that you need to stop shopping as a pastime and find alternate

hobbies. It's very important that you have regular budget discussions with your family,

perhaps monthly. Make it an event that everyone can enjoy as well as be apprised of what's

going on with your family's budget.

You need to keep everybody up to date and remember,

you're going to have to adapt that budget as things change. Very, very important to

not ignore spending problems. You need to address those. In fact, if you find that you

have someone in your family — maybe yourself — who finds that they need to be buying

things to find some type of pleasure, then you need to get some sort of counseling for

that particular individual. I would recommend that you look at your consumer credit counseling

agency for what type of programs they have that can help to prevent those types of problems

from getting out of hand. Also, you need to, as I've said before, stay away from the malls,

stay away from the superstores. You need to go shopping with a list in hand, planning

to buy only those items on the list, and you need to work together as a team — a family

group — that doesn't buy beyond that list.

Also, acknowledge everyone's contribution

to the resolution. And as everyone works hard towards keeping in that budget, you need to

make sure that you praise them. You need to help each other plan outings that aren't expensive,

like going to the park or maybe some low-cost museum visits. And discuss with them the expectations

that you have before you go to a store or before you go shopping. Make sure, especially,

that you discuss this with your younger children so that they'll know they're not getting a

new toy that day, but let them know what you are planning on doing. Again, shop only from

that list and don't attend sale shopping unless you have that list with you. You'll find it's

not so hard to live within your means, and that you get out of debt a lot quicker than

you ever thought possible..

Debt consolidation is a total trap! Or is it? The real answer is: it depends. You see debt consolidation is one

of those really tricky things that if you do it right, it'll save you

thousands of dollars in interest payments and countless headache. That's why you see it advertised

all over the place like it's some sort of magic pill. …it's not by the way.

But if you do it wrong, it can get bad. And I mean really, really bad. I mean thousands of dollars, there

goes your credit, oh wow, there goes your house, kind of bad. And if you don't pay attention to every

little detail about the process from start to finish, you will end up on

the bad side of the deal every time. So today we're breaking down the

pros, cons and pitfalls of debt consolidation, so that you can

make sure that your process is a money saver instead of a money pit. Hey Dreamers and welcome back to

my channel, where we break down all things money so it can stop being

an obstacle and start being what it is: a tool to help you build a life

that you truly find worth living. Now, before we start walking through

the pros, the cons and the pitfalls of debt consolidation, let me introduce

myself to the new folks in town. I'm Tiana B. Clewis, an author, speaker, and coach who

has dedicated her life to helping women entrepreneurs transform their relationship

with money so they can grow their income, dump debt, and start building a lifestyle

that they've been dreaming about…

While still having some fun along the way. Believe me, when I say that you

actually can't eliminate your student loans and take your kids

to Disneyland – although I wouldn't do it right now – at the same time. I've done it and so have my clients. If you want to join me on this story,

like this video and follow my channel by clicking the big red button below. Then hit the bell to make sure you're

notified when I drop new money tips and strategies each and every week,

that'll help you hit your financial goals while still enjoying life. Now let's talk about debt consolidation. First things first, what does

debt consolidation actually mean? Debt consolidate is when you

take multiple debts, you combine them all into a single debt. Once they're combined, you only

have one debt, one lender, and ultimately, one monthly payment. Now the thing is that the total

amount of the debt that you owe doesn't actually go down. But the consolidation process can be

really helpful for a variety of reasons.

Reason one: now that you only have

one monthly payment to make, it's easier to budget and manage the flow. There's no more using calendars and

shuffling around money to make sure that each debt gets paid on time

through the individual portals, only to actually risk missing one and

accidentally failing to pay it on time… because despite the fact that it's

2020 and technology is cheaper than ever, some of the companies

still don't have auto pay options or even electronic payment portals. But with only one that's a

minute, at least all of those concerns are no longer a problem. Reason two, is that now that you only

have one company to deal with, life becomes easier when there's an emergency. If you lose your job or get sick

and can't work for a while, you only have to worry about one company.

And as long as that company has plans

in place to help in times of hardship, you can call up one company to

negotiate with instead of like seven. Reason number three, which is the

benefit that's most important to me, is that if you do it right, you're

going to save money over your repayment period, because you snagged yourself an

overall lowest – lower interest rate. And that's what we always want. But notice that I said, "If you do

this debt consolidation, right." You've probably heard from some

big name money gurus that say debt consolidation is a terrible idea.

Ultimately they say this because

it's really, really easy to mess up. If you do it wrong, you'll end up with

more debt, pay more interest in the long-term, or even risk losing your home. And it's not because people

are just dumb or uneducated. It's just because there are lots of

details that you have to pay attention to. And the folks guid- guiding you through

the process aren't typically inclined to help you see all those details. In fact, in some cases, they'll

try to steer you away from looking at some of them too closely. So that means that you

have to be extra vigilant. Now, before I get into those

issues, I have to take a moment to give you some really important

caveat about debt consolidation. The first caveat is that in most cases,

you can only consolidate unsecured debt. Unsecured debt is anything that doesn't

have collateral – or some kind of material good, physical good – attached

to it that can be claimed by the bank if you fail to pay the debt as agreed to.

Well on a mortgage, the

collateral is the house. That's why banks will foreclose on the

house if you fail a bit in the mortgage. Or on a car loan, the

collateral is the car. Hence the dreaded repo man. Now for a lending institution, a secure

debt is a much safer bet because they have something that they can physically

take away and sell, if you don't pay up. But on something like a student loan,

where there, no collateral, it's just your word that you will pay off the debt.

Now, in the case of debt consolidation,

those loans are typically unsecured. So in many cases, a secured debt,

like a car or a house gets left out of the consolidation process because

the lending institution doesn't want it take on that risk without

adding the collateral in as well. Now, to be clear, there is such a

thing as a secured debt consolidation. So It's possible to get a car

loan, a boat loan, or even a mortgage included in the new loan. However, they're going to want

to that car, boat or house as collateral against that loan. I say all that to say that for

most people, debt consolidation is still going to leave you with a

couple of leftover debts to manage, like the car or your mortgage.

But if you really want those things

included in the consolidation, at least, you know now that you can

specifically look for a lender that offers secured consolidation loans. The second caveat is that the terms

of your debt consolidation loan is going to be heavily influenced by

a combination of your credit score, your income, and what the Federal

Reserve is doing with interest rates. If any of those things is not going

in your favor, like your credit score is going down instead of up,

that consolidation is probably not going to get you in an interest rate

low enough to make it worthwhile. Now, if you want a breakdown about what

should be happening in each of those areas and why, you can check out episode

112 of the Dreamers Financial Playbook podcast, or the video on my YouTube

channel called "To Refinance or Not | When You Should Refinance Your Loan." There, I break down each of those

elements, why they matter, and what you should be looking for. All right, so at this point, I really want

to talk about where things can start to go wrong in the debt consolidation proces,.

But I have one more

thing I have to mention. As I was writing this out, I realized

I have way too much to cover it in order to make this a single episode. As you've likely noticed, I've been

trying to cut my time down from an average of 35 minutes to about 10 to 15. And that's just for the sake

of your attention span and your super busy schedules. That means that this has now officially

become a two-part mini series situation. So be sure that you come back next week

to get more ways in which all of this can go wrong and have to protect yourself. Cool? You good? Alright. The first place where something could

go wrong in the debt consolidation process is when you're choosing how and

with whom to consolidate your debts.

Like everything else in finance, there

is more than one way to skin this proverbial cat, but some of those ways

are super risky and are likely to cost you a lot more money in the long run. And well, you know, me, I am

not about spending more money on debt than you absolutely have to. So I want you to pay really close

attention because I'm about to break down each of these methods,

starting with my least favorite. My least favorite method happens to also

be an insanely popular one: using a new credit card with a 0% introductory rate. If you're using a credit tracker

like Credit Karma, or one of those money management app, like a Truebill

or a Clarity Money, you've probably seen this presented as a good option

for you on multiple occasions.

These companies will often encourage

you to,consolidate your debts to improve your credit score or

to lower your monthly payment. What they don't tell you though is

why credit card companies are happy to give you that 0% introductory rate,

assuming you qualify, in the first place. Now there's a lot of elements to this

that I probably need to do a separate video to break down fully, but ultimately,

most people are not going to pay off the entire balance of the debt before the

introductory rate ends, which they know. The problem with not paying it off before

the introductory rate ends is that you now have to contend with that typical

interest rate of anywhere from 15 to 26%. When you consider the fact that many

personal loans and student loans have rates far below that number,

you can see why this is huge problem. In the long run is going to cost you

thousands of extra dollars in interest. Now here's something else

that can easily be missed. Some of those credit cards that

are advertised as 0% introductory APR is, are not being upfront.

There have been some instances

where the cards making that claim actually deferred the interest

during that introductory year. So if you picked a cart that wasn't

being upfront or clear about its terms, you may find yourself being

hit with a massive interest charge during year two, for interest that

would have been paid on the monthly balances during that introductory year. So for those two reasons, I strongly

discourage anyone from using a credit card for debt consolidation,

even if the interest rate is set at 0% for the first year.

And even if you actually can qualify

for it which most people don't. Another popular method is targeted

specifically at home owners like myself. Some lenders will actually encourage

you to use a home equity loan or open a home equity line of credit, known

as a HELOC, to consolidate your debts. With both of these the banks are

lending you money against the equity that you have accumulated in your home. So the equity is the difference

between how much the house is worth, what others will pay for it and

how much you owe on the mortgage. So if you own a $300,000 house,

have a $200,000 mortgage, then you have a $100,000 in equity.

The difference between the home equity

loan and the HELOC is that the HELOC is a line of credit, similar to a credit card. You can charge up a certain

amount, pay the balance down and then charge it back up. Whichever one you choose, we still end

up with a problem because both of them are using the house as collateral.

So if you fail to make the payments

as agreed on either of those, the lender can foreclose on your house. If you've been following me for a while,

you know that I'm always against anything, that's going to put your house at risk. I strongly believe that if you can at

least keep a roof over your head, you can figure out the rest, like anything

else, during the toughest of times. So when it comes to debt consolidation,

or really anything for that matter, stay far, far away from HELOCs and home

equity loans, because they put your house, where you lay your head at risk. Another method, which I consider

to be far more acceptable, but still again, not my favorite, is a

loan from your retirement account. Most retirement accounts have

clauses that allow you to take out a loan from the account up to a

certain percentage of the balance. It's a way to leverage the cash

sitting in the account without having to actually pay a bunch of fees and

tax penalties for early withdrawals, which we know those fees are no joke. The lovely thing about these loans is

they often have insanely low interest rates and favorable terms all around.

Also you're using your own money,

not someone else's, so when you're paying it back, it's kind

of like you're paying yourself. But if that sounds too good to

be true, that's because it is. There are two many problems

that we have with this one. The first is that the rules of the loans

is governed not only by the institution managing the account, but if it's

through your employer, there can also be another set of rules tacted on by them. That means rules can vary widely and

you need to know all the details fully before you take out the loan and those

details aren't always the easiest to find.

So here's some examples. Now there are some retirement plans that

will allow you to take on a loan at any time, for any reason, up to a certain

percentage of the account balance. But the same plan with the same

institution, but a different employer may have a predetermined list

of when you can take out a loan. Some retirement plans allow you to

pay above and beyond the minimum monthly payments so you can pay

it off early, but some don't. Some require automatic ACH transfers

for the payments while some, let you hit a pay now button when you want.

And for others, you can pay the

entire loan off in a big lump sum early and for others, you can't. So, if you're willing to chance using this

method, read all the rules very carefully and make sure that you actually have all

the rules to read in the first place. The other problem is that you

lose the growth you would have gained while the loan is out.

When you take a loan from a retirement

account, they have to sell off shares of the stocks, bonds, and mutual

funds that you're invested in to provide you with the actual cash. So if those investments go up while

you have the loan out, you've now missed out on the growth because

you sold off those particular items. This is why you're often advised

to just let the money stay in the retirement account no matter

what, because ultimately, the stock market is going to go up. Even in periods of recession,

like now, when you ride it out, the stock market always rebounds. Now it may take a year or two, but I

promise you the sucker's coming back. So again, this method is still better

than the first ones in many ways, but ultimately, it's still not ideal. Another option is for those people

who have a whole life insurance policy with a big cash value. Many of those policies have terms that

allow you to take out a loan against the cash value of the policy, which you

can then use for debt consolidation.

It's similar to the loans from retirement

plans, where you get really low interest rates and often super favorable repayment

terms like the ability to straight up stop repaying the loan, if you want to. Also if your policy is set up right, the

cash value of the policy will continue to grow even while the loan is out. If you've ever heard anyone talk

about being your own bank, this is exactly what they're talking about. In fact, you can get more information

about this concept, an episode 82 of my podcast or look for

"Demystifying Self-banking with Mark Willis" on my YouTube channel. I interviewed him. We talked all about the

concept right there.

Now, remember that I said, if

your policy is set up right. It's actually one of those warnings that

Mark put out there in our interview. There's a lot of insurance brokers

out there selling policies that claim they have these features, but

aren't actually set up properly. As a result, there can easily be

hidden fees and even tax penalties when you take off the loan. So once again, you have to read all of the

fine print so that, you know the rules.

We're down to the final method, the

one that I actually recommend for you, if you really want to do debt

consolidation in the safest way. Just go to a bank that you trust and get

a personal loan with a low interest rate. Now I'm a fan of using credit unions and

local regional banks because they usually give better interest rates and terms than

the big national and international banks. But notice I said usually not always. Either way, you're definitely going

to want to shop around on this one. Now under their personal loan options,

it's common for a bank or lender to have a debt consolidation option. What usually ends up happening is that

during the process of getting the loan, the bank gathers information about all

of your debts that you want to pay. And if you're approved and agree

to accept the loan, the lender will pay off all those debts on your

behalf, leaving you with just the consolidated loan from that lender. Now, as I mentioned before, there

are options for secured debt consolidation, where you have to

put a collateral for the new loan.

In those cases, you ideally wants

to include your other secured debt into the consolidation and use

the collateral from the old debt for the new consolidated debt. That's just the simplest

way and safest way to do it. You also want to make sure that you're

going to get a fixed interest rate, that at the end of the loan, you're

going to end up paying less interest, and a bunch of other things… which is exactly why there's

going to be a part two. So, as you can imagine, I'm going to

stop right here because I've already given you a lot to think about

when it comes to understanding debt consolidation and what your options are. The last thing I want to do is

overload your brain with too much debt consolidation information too fast.

So we're just going to give you

a little time to think about it and let your mind rest for a bit. But I still want you to get

the rest of the information. So join me next week when we dive into

several ways, you can avoid taking on more debt or paying extra interest during

and after the debt consolidation process. But before you go, I wanted

to talk to you about something that's pretty darn important. For some of us, things like refinancing

loans and debt consolidation end up sounding super tempting because we think

that if only we could get ahead on these dag-gone debts, then we'll be fine. But as you've probably picked up

during the video, that may not be the best game plan for you. It can easily go wrong. But you still find yourself

entertaining the idea, because honestly, you don't really know where

to start to fix your money woes.

So you're really guessing on

whether you need to focus on the debt through consolidation,

refinancing, or something else. The truth is you might

have an income problem. Or it could be that you have a sale things

problem that just won't let you be great. Or maybe it really is the debt. Well, it's time to stop guessing. I've pulled together a quick guide to

help you pinpoint exactly where you should focus your financial efforts,

because when you know where to focus first, you can eliminate all those random

attempts that get you absolutely nowhere. To get your hands on my free

guide, I want you to head over to tianabclewis.com/sanctuary and join

the Dreamers Financial Sanctuary group. That's a Facebook community of a

fellow women entrepreneurs using their hard-earned cash to dump debt, save money

and create the life of their dreams. You'll easily find the guide pinned to

the top of the group for you to download. Also, don't be shy. Go ahead, introduce yourself in the group.

The group members and I would absolutely

love to get to know you on your journey as we are getting super focused

and making things happen together. But wait, before you head over to the

group, let me know that you found this video useful by hitting that thumbs up

below and subscribing to my channel. Don't forget to hit the bell so you're

notified each week when I drop brand new money tips or strategies that are going

to help you use your cash to do all the things we just talked about: dumping debt,

saving money, building your daily life and doing it without sacrificing all the fun.

Finally, if you're looking for more information

that will help you transform your debt into a distance memory faster

than you ever thought possible, these videos are exactly what you need. With that you get to watching these

videos and I'll see you next week. Bye bye..