Meet Tom. Tom is a few years out college with a great

job and a lot credit card debt. Tom wants to get out of debt, but isn’t

quite sure how. Luckily for Tom, there exists a great solution

to his problem: balance transfer cards. However, before we continue, if Tom doesn’t

have a firm understanding of what a credit card or credit score is, or how to effectively

use either, we highly recommend watching our three videos “Credit Cards 101,” “Credit

Scores and Reports 101,” and “Credit Cards: Mistakes and Best Practices” before continuing

further. But let’s get back to the matter at hand. What is a balance transfer? Well, a balance transfer is simply the act

of transferring an existing credit balance to another credit card.

Most credit cards aren’t good this for:

they’ll immediately start charging interest on the transferred balance, plus a fee, generally

about 3-5% of the transferred balance. However, there is a specific subset of credit

cards, called balance transfer cards, that won’t immediately start charging interest,

instead giving Tom a 15-21 month window of 0% APR to pay off his balance interest-free. This is a great deal, but let’s still walk

through the steps you’ll need to take to get one: Step 1: Before doing anything, make a debt

repayment plan, ideally using our free recommended website, and rank your credit cards by interest

rate, as no matter what you end up doing, you’ll always want to tackle the highest

interest rate debt first.

Step 2: Once that’s done, call your credit

card company and try to get them to lower your APR. Emphasize that if they don’t agree, you’ll

move your balance to another company offering lower rates. Step 3: If the call fails and you still want

to transfer, keep in four three things. One: You’ll need good credit to get a balance

card. Two: You can’t transfer a balance to a card

offered by your current bank. Three: Depending of the size of your debt,

you may not be able to pay it off by the end of the promotional period, so have a plan

for that.

And Four: The credit line on your balance

transfer card may be below your total debt load, meaning you’ll either have to:

Apply for a second balance transfer card Keep the remaining debt on your current card

and pay the high rate. Or use a personal loan, which is slightly

more expensive than a balance transfer card, but comes with a lower credit score requirement. And don’t worry, we’ll cover this option

in our next video. However let’s assume for now that Tom has

been approved for a balance transfer card with a high enough credit limit. This is an important first step, but they’re

still a few more things to keep in mind: One: Don’t spend on the card, as the 0%

APR period may not extend to purchases. Two: Complete the transfer as fast as possible

or the 0% APR offer may expire.

Three: Be careful about consolidate multiple

balances onto one card, as that will lower your credit score. Four and Finally: Once you’ve completed

the transfer, always pay on time and don’t close out your old accounts, as failing to

follow either will lower your credit score. Hopefully you and Tom now better understand

balance transfer cards. Be sure to check out our next video, where

we’ll teach you how to get out of credit card debt without them, and be sure to website,

where you can find more educational content, your free credit score, and great credit card

recommendations..

Meet Tom. Tom is a few years out college with a great

job and a lot of credit card debt. He wants to get out of debt, but isn’t quite

sure how, especially because he didn’t qualify for a good enough balance transfer card, detailed

in our two-part video series “How to Get Out of Credit Card Debt”. While Tom may think all hope is lost, there

is another way: personal loans.

However, before we continue, if Tom doesn’t

have a firm understanding of what a loan is, or how to effectively use one, we highly recommended

watching our two videos “Loans 101” and “Loans: Mistakes and Best Practices” before

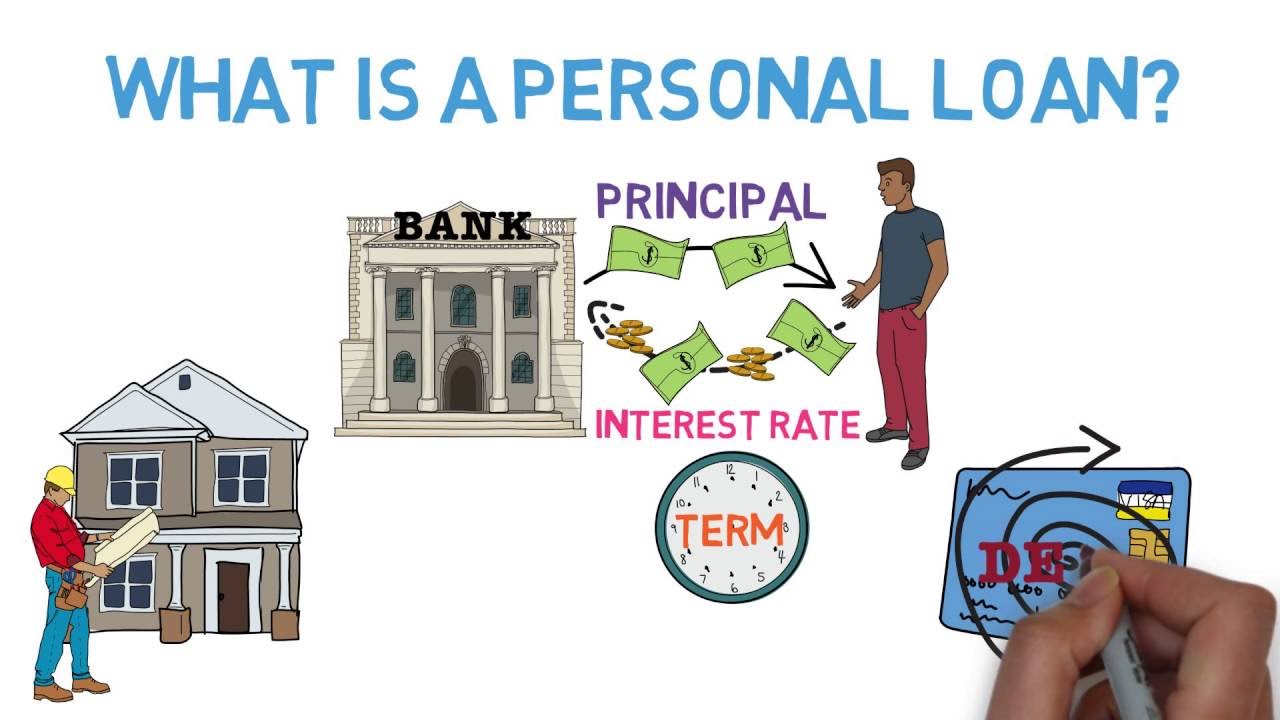

continuing further. But let’s get back to the matter at hand. What is a personal loan? Well, like most loans, personal loans offer

Tom a fixed amount of money at a certain interest rate for a set period of time. However, unlike most loans, personal loans

can be used for a wide variety of expenses, ranging from home improvement projects to

paying off credit card debt.

Speaking of credit cards, personal loans,

especially those from online lenders, will have interest rates lower than almost every

credit card. In addition, if Tom borrows from an online

lender that considers not just his credit score, of which he’ll need at least a 640,

but also his education status and earnings potential, those interest rates can be even

lower. Plus, even better, applying for a personal

loan from an online lender couldn’t be easier. All Tom needs to do is fill out a short credit

application. Then, the lender will likely use a “soft

pull” for his credit history, which won’t hurt his credit score, and within a few minutes,

Tony will be able to see the amount see can borrow and the APR he qualifies for, a process

he can then repeat at multiple online lenders. Should Tom instead choose to get personal

loan from an offline lender, like a big bank or credit union, which just have one warning.

These institutions tend to have higher interest

rates due to their much greater overhead, plus they tend to avoid “soft-pulls”,

which makes it harder to check your rates without hurting your credit score. So let’s assume Tom has chosen to get a

personal loan through an online lender. What’s his next step? Well, assuming he’s chosen his lender and

has checked his rates, he can then fill out the actual loan application online.

This should be very simple process, but there

is one thing to watch out for. Online lenders often charge a nonrefundable

origination fee for creating the loan, generally ranging between 1-5% of the loan’s value. This generally means two things:

One: If Tom wants to borrow exactly $10,000, and has to pay a 1% origination fee he’ll

need to borrow $10,100 dollars instead. Two: If Tom wants to use the loan proceeds

to pay off credit card debt, he needs to make sure the origination fee is less than the

interest he’ll save by using a personal loan. And don’t worry, our online calculator makes

this process a breeze. Finally, assuming the math checks out, Tom

just needs submits his application.

At this point, there will be a hard credit

check, but assuming Tom is approved, his bank account will generally be funded within a

few days. Tom is now on his way to being debt free. Congratulations! You’ve finished our personal loan basics

curriculum! If you want to see our free recommendations

for personal loan lenders, or just check out more educational material, be sure to check

out our website!.

Hey, it's Jesse Eker! and I'm excited for you to

watch this video right now. Now, when I was young,

my dad, T. Harv Eker, taught me this really important lesson. My dad came up with the 6 Jars System. It has worked wonders for thousands upon thousands upon thousands of people to not only get more in

control of their finances, but also help them actually

become financially free. Now, we've created this worksheet for you You can fill it in online,

or you can print it out. It's gonna actually take you

through the 6 Jars System so that you can

personalize it for yourself and see how it works. Now, the Jar System is just

a money management system which is six different jars. And the jars are a metaphor, okay? We like to use jars because

you can actually see them. You can see the money pile up. But now that online banking is so big and there's lots of

different advancements, you can always open

different bank accounts, and that's what I personally have.

When you make your money,

100% of your money, you divvy up into the different accounts. What that does is Your things that you need to survive. Things that you just wanna blow money on. Where you are giving back to charity and contributing. Where you can pay for investing in yourself and in educating

yourself to a higher level. This account is geared to help you become financially free. And so you have these different accounts that you use all the time. When you get the money, you then divvy it up

through the different jars. In Harv's system, he

has specific percentages that you put into each jar. One of the most common

questions that we get is, What I need to at least express to you is Once you get in the habit

of managing your money, once you started making more of it, you continue to stay in that habit.

There's a really great example

of someone named Michelle. Michelle came to Millionaire Mind when she was dead broke. She had basically no money. And so, she learned the Jar System, and what she decided to do

was, she decided to manage $1. She took $1, and she split it

up into the different jars. Then the next week, she took $2. Then the following week, she did $5.

Then the following month, she did $10. Then the following week, she did $20. It continued to escalate. And

she did every month or week, but she kept doubling it. By the time, by the end of the year, she was managing a thousand dollars. And now, guess what? She's a multi-multi-multi-millionaire because she was able to

not only manage her money, but she was able to invest

her money really, really well. The ways that we taught her. And she continued to make a lot of money. Then you don't run out of money. Then everything that you do

has a designated place for it. Holidays come up. You

have a designated place where that money is stored. You want to buy something for yourself. Well, is it something that's impulsive? Use your play account. Rent's coming up or your

mortgage is coming up. You have money set aside for that. You never have to dig into any other area. This is where you wanna go

with managing your money. I gotta say, when I finished college and started to self-fund myself… when my dad cut me off and said, "It's time for you to get a job and time for you to make your own income," and stuff like that, I said,

"Okay, that's totally cool.

I'm ready to get going." That's when I started

heavily managing my money. I can't tell you how

much of a blessing it is to have that money managed. It's not only a control thing, where I feel so much more

secure with our finances, but it feels good to know that I could go on a 21-day vacation and I have that money already set aside, and it doesn't affect

anything else in my life. That's because the way

we manage our money. We have done extremely well with our finances because

we manage our money.

For the last couple

years, about eight years, we've been taking almost 35% of our income and investing that money

into different income streams and different investments. Last year, we looked at our net worth, and it was over a million dollars. That's because we managed our money. If we didn't take that money, if we didn't take that percentage, then we would not be able

to have that net worth. That money could be gone. It could be blown in different areas. So, managing your money

is so, so important, and is really the biggest difference between successful and

unsuccessful people. So right now, I want to encourage you to download the 6 Jar worksheet to fill in your own personal Jar System and create it for yourself.

Right now, I'm gonna

answer a couple quick, common questions that we

get and hopefully help you through some of your

questions that you have. So, the first question that

we get all the time is, what if I don't have…

one of the guidelines for the necessities is 55% of your income should go to your necessities. which is very common by

the way, so don't feel bad, especially when you're starting this. I really want you to really understand I'd rather you manage $1 than stress about the percentages. The percentages are there as a guideline for you to look at and

for you to work towards, but it doesn't mean that

you can't manage your money without starting that, right? Think of it, the habit is more

important than the amount, and you can get there as well.

Now, another common one is debt. So, what if you have a ton of debt? Again, it's managing

your money is the habit more than the amount. If you have debt, what I would do is you take one of the jars, which

is your long-term savings, and I would probably split that

up into two different jars. One goes for your debt, and one goes for your actual savings. So, instead of putting $50

into your long-term savings, you're putting $25 towards your debt and $25 towards your savings. Now, why not pay off your debt first before you manage your money, right? Well, that is a mistake because what happens when you pay it off? Well, you're not in the

habit of managing your money. But Jesse, I will manage your money. Yeah, right. How is it working so far? Have you done it up to this point? Managing your money is

probably not new to you.

Maybe this system is, but you're probably not

new to managing your money. What I say is get in a habit first, pay off your debt a little bit later. Who cares? At least you're in the habit. Then when you've paid off your debt, you're in the habit of managing your money in a very structured, systemized way that's going to help you in your future. Another question that

we get all the time is You don't manage your

money with your business with the Jar System. In business, you pay yourself a salary or you pay yourself a profit distribution. However you do it. So, the business is very different than what you do in the

Jar System, all right? Personal finance is

different than your business. Another one that we get all the time is, Every relationship is different. Every person is different. But here's how me and my wife, Jen, do it. We share our money. Some people don't, which is totally fine,

but we share our money. Our main jars are all together, so we have all of our main jars. The one jar that we have

different is called the play jar.

That play jar is basically where we have our own jars to play with. So, if Jen decides that

she wants to go buy, let's just say, a purse, and it's ridiculous in

price in my perspective, I can't say anything about it because that's her own play money. If I decide to go buy myself a nice watch because I wanna blow that. Or I want to take a

trip on a private plane. If I really wanted to do

something crazy like that, she can't say anything

because that's my play money. What that does is it gives flexibility, it doesn't give any

judgment, and it's fun. It's like you can use that

play money for yourself, and there's no judgment together. Now, you can also set up a play account with your family, as well,

for you guys to do together. But I really, strongly recommend that you at least set up

two different play accounts so that you guys can not have any judgment on what each other are spending.

The way that we do it is we put everything on our credit card because we have great money management. If you don't have good money management, I wouldn't start with credit cards. But if you have good money management and you're disciplined, what we do is we put

everything on one credit card that we get a ton of points with. We use the credit card to our advantage to get the points. Now, every couple weeks, we go through the credit card statements, and we write next to the statement

what jar it comes out of. Is it necessities? Is

it a long-term saving? Is it one of our plays? We write it down, we tally it up, and then we go ahead and take

it out of that Jar System. We do that on a consistent basis. We never have any balance

on our credit card left. It's always zero for us. Now, one other question that we get is the financial freedom account. Well, it kind of can go

to your own discretion. It could come out of long-term savings, or it actually could come

out of financial freedom because the business is gonna actually help you become free, right? I wanna just clear something up.

These are guidelines that you can follow. If you're having trouble figuring it out, just put it in a jar. Put it under there. Whatever feels good for you, as long as you know that

you're managing your money, you're not taking advantage, and you're not trying

to shortcut the system. Just be flexible with it. Don't be so rigid with it. If you're not really sure, pick one. You're not gonna get it wrong. Which then helps you when

you're making more money to then invest your money

and become financially free. Another question we get is

your financial freedom account. We encourage you through our FreedomFirst

Wealth Coaching program to invest in passive income vehicles, vehicles that are going to

pay you on a consistent basis without you actually needing

to spend time working in those vehicles or those investments.

So, what do you do with that money? Do you pay for your lifestyle

or what happens with it? If you wanna become

financially free quicker, then you wanna invest your money quicker. Like I said, over the

last seven-plus years, we've been putting 30-35% of

our income into investments. And we now have a net worth

of over a million dollars because we continue to do

it over and over again. We don't use that money ever. We use our business to make our money, and we use our investments

to invest our money. We keep it and enroll it, and that's how you grow your wealth and how you continue

to become free quicker. I recommend to at least

put it back in there, compound, let it grow,

become financially free, and then make that decision.

All right? So, all of this is coming from our FreedomFirst

Wealth Coaching program, that is very unique into helping you get on the fastest track to

creating financial freedom. In those pillars, there's

lots of different elements. There's multiple different elements that we work on within that program. We're actually gonna be

taking our next group of students in the next week or so through this eight-week coaching program. This coaching program's

only open two times a year. You will be closer to reaching

your financial freedom than you ever have – ever

– in your whole life. We are going to be working

on all the different elements that you need that are crucial

to becoming financially free. We've had thousands of students

go through this program and absolutely love it. If you are interested in that program, then go ahead, and

there's going to be a link below the worksheet, as well. There's gonna be probably a

button below the worksheet, and that is going to

give you more information about the FreedomFirst

Wealth Coaching program.

There are seven more that we

work on with our students. By the end of this program, you will be on the fast track to freedom. Thanks for watching this video. I hope you enjoyed it. I hope it cleared up some

information about the Jar System, but the most important thing

is to start doing the jars now. You're never too early.

You're never too late. I started my first one when

I was, basically, born. I ended up stopping it

when I was in college, when I was not really making any money, and I didn't really follow the system because I was "too cool." But really quickly learned again that I needed to do the system. We have lots of kids who…

parents who start it for

their kids at a young age. We have lots of people in their 70s who started right then and there. The goal is to make sure that you become financially

free by managing your money, because all the different

ways of the system work to help you expedite that freedom. Thanks again for watching this. Hope you enjoyed it, and have

a great rest of your day..

debts snowball and debt avalanche are two of the most famous go-to methods for getting out of debt both require you to focus on one debt while making the minimum payments on all the rest however the debt you focus on is different for each method let's find out which method of debt reduction suits you better [Music] using the debt avalanche method you make the minimum payment for all your debts but focus on the one with the highest interest rate you save you big guns for that one any and every extra dollar goes towards paying off that high interest debt once the big one crumbles and crashes you move on to the next biggest and so on until you're debt-free money was this is the smartest solution since you're getting rid of the debt with the highest interest rate first with the debt snowball method you completely disregard interest rates the only thing that matters is being able to take your debts off quickly which is why you attack the smallest debt first for making your minimum payments on all the others once you're done with the smallest debt you can add the money that went towards your snowball and move on to the next one your snowball grows with every debt you pay off sounds sensible right well it is but it will almost certainly cost you more than the avalanche method especially if you have debts with high interest rates so why do some people prefer it over debt avalanche because each small victory gives you a morale boost that's your fuel to keep going the debt snowball method gives you visible results quickly for many people that feel-good factor makes it worth paying a little bit extra in the long run debt avalanche is undoubtedly the more sensible approach but sticking to it requires more determination there are no external motivators so you need to keep pushing yourself to make your payments so have you ever used any of these methods or did you approach your debt in an entirely different way let us know in the comments [Music]

Meet Jasmine. Jasmine is a college student attending State

University. Like many college students, Jasmine has a

lot things she needs to buy: books, laundry baskets, food, and so on, and she can pay

for those things with two types of money: debit or credit. Debit is money that comes from a personal

bank account. Credit is money that is lent to you by your

bank. For example, let’s say Jasmine has been

using a credit card. Each time Jasmine uses the card to buy something,

say a $100 textbook, her bank is loaning her the money. While that sounds nice, be warned, the bank

isn’t giving Jasmine this money for free. They expect her to pay a certain amount of

money each month, called interest, if she doesn’t totally pay off her balance by the

due date.

As you can imagine, this can get very expensive

very quickly, especially when factoring in the high annual interest rates, or APRs, that

are charged by these companies. However, there is a solution to this rather

scary problem. As long as Jasmine always pays off her balance

in full by her monthly due date, she’ll never pay a cent of interest. Jasmine is shocked and thrilled, but still

isn’t quite sold on credit-cards. After all, with all their flaws, are they

really worth using? The short answer: as long as you avoid running

up a balance, definitely! So why is that? Well, “free money” for starters. Most credit cards offer their users rewards,

like cash back or airline miles, each time they make a purchase. For example, let’s say Jasmine’s credit

card comes with 2% cashback. That means if Jasmine spends $500 per month,

then at the end of the month she’ll automatically get $10 back, no questions asked. Then, if that wasn’t good enough, responsibly

using a credit card also allows Jasmine to build a great credit score.

This is a calculated number between 300 and

850 that summarizes your credit history, covering everything from your payment history to the

age of your accounts. While we’ll teach you more about your credit

score, including how to get and improve it, in our next video “Credit Scores and Reports

101”, just for now know that most credit cards actually require a credit score of at

least 600, plus at least $15,000 in annual income and a reasonable debt payment to income

ratio, generally below 36%. However, thankfully for Jasmine, who lacks

both credit history and a full-time job, she shouldn’t have a problem getting a student

credit card. In fact, the online application will take

all of five minutes. She’ll just have to be a full-time student

of at least 18 years of age, with either a small amount of income, like from a part-time

job, or a creditworthy co-signer. However, at this point we have to say, be

careful. Taking on a co-signer is no small matter. The account is still in your name, so any

credit mistakes are on you and your co-signer, plus your co-signer is even liable for any

of your missed payments.

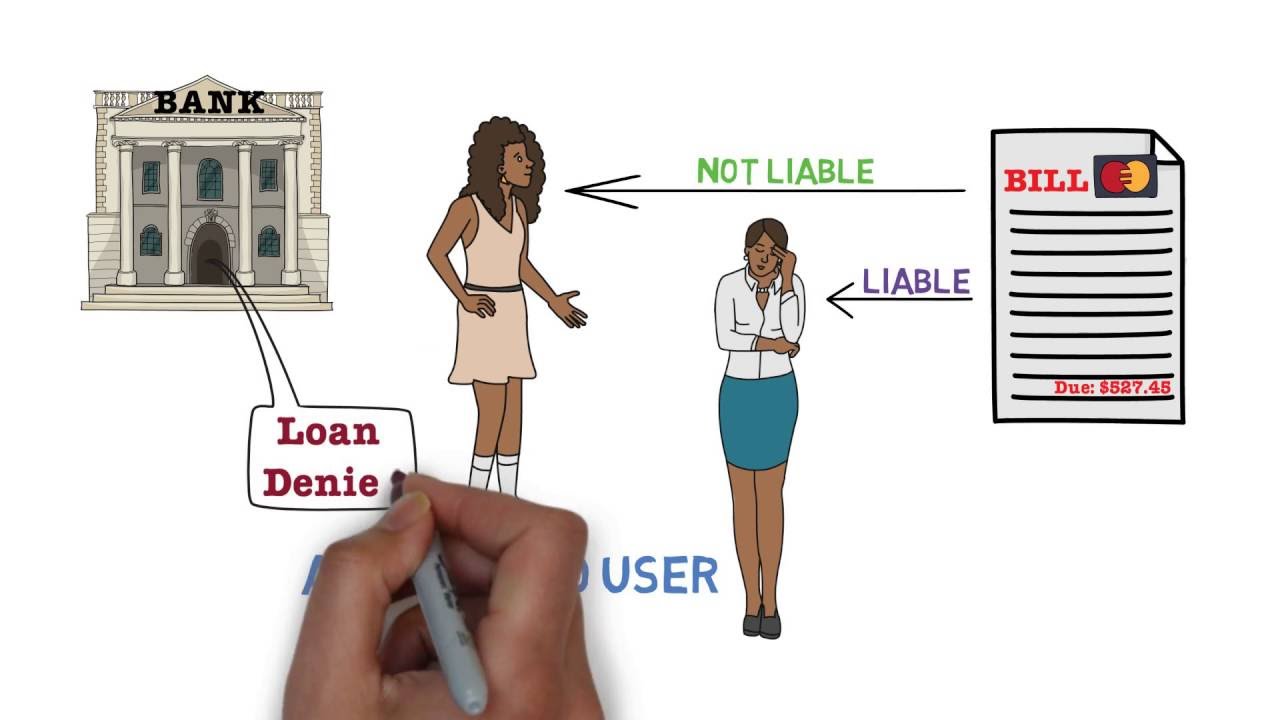

If Jasmine isn’t quite ready for that level

of responsibility, she can instead be added as an authorized user to her family’s account. Not only will this allow her to get her own

credit card, but in a few short months the credit bureaus will treat her parent’s credit

score as her own. Sounds pretty great right? Well, this strategy isn’t a cure-all.

Even though Jasmine isn’t liable for payments

on the account, her parents still are, plus many lenders will want to see you successfully

handling credit on your own before giving you a major loan. Hopefully you and Jasmine now understand the

basics of credit cards. Be sure to watch our next video, which covers

everything you need to know about credit scores, and be sure to check out our website, where

you can find more educational materials, your free credit score and great credit card recommendations..

Hello, friends! I know you are expecting a video on the Pegasus Scandal, But I'd like to wait for a few more days. It's very recent news with

new developments are surfacing every day. So let's wait for a few days. And then I'd make a video on that topic. In today's video, I'd like to continue with the

Financial Education series. The topic of today's video is,

Credit Cards! What are credit cards? How do they work? How do credit card companies make money? And most importantly, Should you be using a credit card? What are the pros and cons? Come, let's find out. Let's use an example to understand. Suppose you're a school student

and suddenly there's a pandemic. All your classes are now online. But to attend these online classes, you'd need a smartphone, but you don't have one. You need to buy a smartphone urgently. But there's insufficient money

in your bank account for buying it. So you ask your parents to

transfer some money to your bank account.

But it'll take 2-3 days to transfer the money. But you need to buy the smartphone

before your class the next day. What other options are there? In such situations, you can use credit cards to make the purchase immediately. And pay for it later. So essentially, a credit card is a card that helps you in purchasing things instantly. But you can pay for them later. At the end of the month. Generally, if there's enough money in your bank account, you withdraw cash and use it to make payments. The second option is to use a debit card. It is directly linked to your bank account. When you make a payment through your debit card, then the money is deducted directly

from your bank account and transferred to the other party. But in a credit card, the bank makes the payment on your behalf. To whomever you're trying to pay.

And then at the end of the month, you repay all the expenses of that month to the bank. You can take more than a month in

repaying the bank's money. Then the bank will charge high interest. Similar to a loan. So you can think of the credit card

as a type of a 'mini loan.' Normally when you take a loan, you can get it in cash if you want to.

But here, instead of a loan,

the bank is giving you a plastic card. With your name and a unique number on it. So that the card can be uniquely identified. As well as the expiry date. How is the payment being processed? There are some payment processing companies. Like Visa and MasterCard. These two are the most popular companies. They basically provide the back-end infrastructure to facilitate credit card transactions. The bank issuing you the credit cards, are distinct from Visa and MasterCard. These two are only involved in the payment processing.

And there is a magnetic strip on

the other side of the credit card. As well as the CVV number. It is very important to keep it safe and secret. Otherwise, you may be a victim of fraud. Now, friends, every credit card has a credit limit. The amount of money that

you can spend with the credit card. Without first paying the bank. If the limit is set at 30,000 Then you can't spend more than 30,000

using that credit card. The credit limit varies from bank to bank. And the type of card you've bought. And the bank checks your salary. It checks your credit score. And decides on your credit limit based on these. If the bank is assured that your salary is adequate that you can afford to pay back the bank then the bank will trust you more.

And you get a higher credit limit. Now, Credit Score is also an interesting concept. If you don't make the credit card payments and loan repayments on time, then the bank will think that it will be quite risky to give you money. It'll be unsure about when you'll repay the advances, if at all. Because the bank takes a risk while giving you a credit card or a loan, to judge this risk, the banking sector has created its grading system.

It grades you. The score ranges from 300 to 900. And it is known as your Credit Score. If your credit score is between 750 and 900, then it is an excellent credit score. It means that the bank can trust you and the risk is very low. But if your score is around 300-400, then the bank can't trust you at all. So your credit score is calculated

based on your previous track record. And on that basis, the bank judges if your credit limit should be high or low.

In fact, whether or not to issue a credit card to you at all. How will you benefit from using a credit card? I talked about one advantage at the beginning of this video. That if you want to buy something immediately, but you want to pay for it later at the end of the month, you can. It helps to meet immediate expenses. The second major advantage is that using a credit card is less risky than using a debit card. If you're a victim of a fraud then in the case of a debit card, the money will be directly deducted from your bank account. But in the case of a credit card, your bank or the credit card issuer will pay on your behalf. And if there's a fraud, they can investigate it. If there's actually a fraud, then they'll get your money back. In India, if there's any fraud with your credit card then the customer's, i.e.

Your, liability is zero. If you report the fraud within 3 days. So the risk of making payments is borne by the bank. The third major advantage is the rewards that you get for using a credit card. The reward systems vary depending on

the bank and the type of credit card. In some, you may get cashback in others, you may get heavy discounts you may even get insurance in some. Like insurance to be paid if you meet with an accident. You can also get travel insurance for free with your credit card. The benefits that you'd get for using it

depends on your credit card. But nowadays, almost every credit card comes with some sort of a reward point system. You can collect the points and can then exchange those points to

buy something expensive. Which credit card is right for you? To decide, you need to remember three main things. First is the bank that will issue your credit card.

Any reward point system, the fees charged by the bank and any hidden fees. These are mostly decided by the banks. Second is which of the credit cards offered by the bank will you be using? There are more rewards for high-level credit cards. The insurances and points are also better. But they often have high fees as well. And the third thing to remember is that which payment network is used in that card? As I said, Visa and MasterCard are the two most common networks. But apart from these, American Express,

Diners Club and RuPay are also used. Although Visa and MasterCard are so common that there is a negligible difference between the two. But if you see American Express, then it differs a lot from these two. Because in most of the places Visa

and MasterCard are accepted but not American Express. But American Express offers better rewards.

I told you that banks decide the reward point system mostly but to an extent, the payment networks also decide about the types of rewards on their network and the benefits to the credit cardholders. Although, it is interesting to note that no more MasterCard cards can be issued in India Because MasterCard violated some guidelines and the RBI notified that though people can keep using the existing MasterCard cards but no more MasterCard cards can be issued.

As long as the MasterCard company does not comply with these guidelines. But overall, the various banks it's equally interesting to note that all of them use a different proportion of MasterCard, Visa and American Express cards. On this chart, you can see which banks use which payment network the most. Banks like RBL and Yes Bank use MasterCard exclusively; 100%. And then there are banks like Kotak that use Visa exclusively; 100%. Since we're talking about banks, let's look at things from the bank's perspective as well. How do these banks profit from credit cards? The most simple way for the banks to earn money is by charging annual fees.

To use some credit cards, you have to make yearly payments. Apart from this, there are many different types of fees charged by the banks. If you are not making timely payments, then a late fee will be charged. If you want to withdraw cash from the credit card, then there is often an extra fee @ 2% – 5%. But friends, you'd be surprised to know that a large portion of these banks' income actually is a result of people's stupidity. Many people don't pay their credit card bills at the end of the month. Because of this, the banks charge a high interest rate on it. And this interest rate can be as high as 30% compounded annually. That's twice or thrice the interest rate on loans. The bank earns a lot of money by charging so high interest rates. And people lose their money. If every person using a credit card, starts paying the bank on time then a major part of the banks' profit will disappear. This is the reason why credit cards aren't popular in some countries. In many European countries, credits aren't used much because the mindset of the people is so that they make all their payments on time.

They don't buy anything if they don't have the money for it. People don't really buy things on EMI in Europe. So credit cards aren't very popular in Europe. As compared to countries like India and the USA. Where people have the habit of buy things even when they don't have enough money. That's why in European markets, alternative banks like N26 and Revolut are gaining popularity. They offer some of the functions of credit cards. These banks issue their debit cards an annual fee is charged on some of them and those debit cards offer rewards like

insurances and stuff.

But the security that you get in a credit card is not offered here. So they're trying to offer some of the functions of credit cards. Similarly, some credit card 'challenger' companies are gaining popularity in India as well. Like Slice. It does not charge an annual fee but gives the user rewards as well as security benefits that one gets in a normal credit card. They offer some other advantages that a normal credit card doesn't. Like their 3-months repayment duration. Whereas a normal credit card's repayment duration is normally 30 days.

They claim that they do not have any hidden charges. This specific company, Slice, works only on Visa. It will be interesting to see how with time, the advantages offered by the credit cards the companies are trying to offer these through various channels in the future. And reduce the disadvantages of credit cards. When the competition among these companies will rise the advantages for us will increase and the disadvantages will reduce. But if we talk of the present, the disadvantages of credit cards might already be evident to you. As I've said, if you don't make the payments on time if you don't pay your credit card bills on time, Then you'd have to pay heavy interest. And fall into a debt spiral very quickly.

Where once you don't make the payment on time, then so much interest is charged that you end up paying a higher amount. You wait for a few more days and the amount increases further. Soon, within some days, or maybe a few months, the amount may become so large that you can't repay. I've also talked about the second disadvantage. There are many hidden fees on credit cards. So the question arises Should you use a credit card? Or should you not? The answer to it is very simple friends. If you make timely payments of the credit card bills, then you can use it. On the other hand, if you use credit cards to buy things that you can't afford, if you think that now I may not have the money, so I'll use the credit card to buy it, and I'll arrange the money from somewhere within 30 days, then please don't use a credit card. You may fall into a debt trap. Third, if you want to get a credit card because of the rewards, then evaluate the situation a bit.

The various fees that you will pay to use that credit card, often the processing fee is around 2% -3%, and the reward that you'd get in exchange, would they actually be worth it? Or are you still losing money? So you'll have to calculate it a bit. Fourth, if you're wary about paying online or anywhere else about falling for a fraud, then use credit cards in such situations to be safe. I hope you found this video informative. Here, I would like to thank the KUVERA app for sponsoring this video. It's a wonderful app for mutual funds where you can invest your money in various mutual funds. By setting your goal. Whether you want to buy a house or a car set this goal on the KUVERA app and the algorithm of this app will tell you which mutual fund will be best for you to invest your money in.

Not only mutual funds but you can compare FDs also. What are the rates of interest on FD

given by different banks? The link is in the description below. Definitely check it out. Comment below the topic that you want the next financial education video to be on. Let's meet in the next video. Thank you very much!.

(upbeat rock music) – He sees it, he

wants it, he buys it. – Four cars in four years? What is up with you? – I know what's right,

I know what's wrong, sometimes I just

don't give a (bleep). – Do you have any idea

what I'm gonna make you do? – Get the hell out of here.

– I am serious. (couple laughing) (upbeat rock music) ♪ Money money money

money money money money ♪ ♪ Money money money

money money money money ♪ ♪ Money money money

money money money money ♪ – My name is Candice. I am a secretary for

an education institute. – My name's Clint, I'm

an operations coordinator for a liquid bolt company. Me and Candice

got married young, pretty sure we got

married when we were 22. We think we're coming

up on five years. – Clint never stops spending. – When I get something in

my head and it's something that I want, I don't think

about it and I just do it.

– I don't wanna be

spending the money but he has to buy

everything new. Big screen TV- – Nice definition. – [Candice] He had to

get the surround sound. – Can't have a TV

and not proper sound. – Various video game

consoles in the past, motorcycles, cars,

everything he wants he gets. – Candice definitely monitors some of the spending

that I've done. – There's online banking and I

can view that at the instant. Like where he has gone

to the strip joint. – She'll be online,

she'll be like, oh you're there are you? She's like a stalker like- – Guess who showed up there?

(Candice giggling) Some days I hate

him but I love him. Clint doesn't open any bills, nor does he go online

to check anything. – I have no clue as to

what's in the bank account.

The bill fairy comes

down and pays our bills. (Clint chortling) – I will pull from

our line of credit or go into overdraft. – But that doesn't bother me. Credit is pretty much what makes the world go

'round I guess I would say. – [Candice] Now we

have purchased a condo that closes in a couple months. – Again, that was

probably more my idea. – Clint doesn't realize that we have to come up with

the deposit before we move in. There's other things that

contribute to being emotional. He can't have kids naturally. That's extremely

emotional for me. I'm frustrated, I can't do IVF

because of Clint's spending. – I think mine and

Candice's relationship is more at risk with the baby situation than

the debt situation. – If we get further

and further in debt, I think that Clint and I

will eventually part ways. Because we won't have kids which is something

that I really want. He'll have all his stuff

but he won't have me. (upbeat rock music)

(cars honking) – [Narrator] This month, I'll help this couple

move from red to black.

I've been solving money

problems for over 20 years. Tackling everything from

high finance to low income. I help people understand

money and debt which is still a huge

mystery for most folks. And it's the number one

reason couples split up. So now, I'm making house calls. (upbeat pop music) When it comes to spending, Clint is like a kid

in a candy store and Candice is powerless

to stop the binge. The way things are going, they can't afford

to start a family. It's time for these two to

get their priorities straight. Hi, Gail Vaz-Oxlade. – Hi I'm Candice! – Nice to meet you!

– Nice to meet you too! – I'm Clint. – Nice to meet you Clint.

– Nice to meet you.

(upbeat pop music) – You're a bit of

a boy, right Clint? You're a boy man, you sit here and you

play shoot-em-up games! (Candice giggling) So Clint, how many

hats do you have? – Pardon?

– One, two, three, four, five, six, seven,

eight, nine, ten, 11- (air whooshing)

– We'll go to a store, Clint is like a woman, he will

try on fifty million things. He's got a hat fetish,

shoes, clothes, everything. – One of the things that I

notice about the two of you is that there's a definite

discrepancy in your stuff. His robe is beautiful. – Oh yeah.

– Her robe is ratty. – I'm sorry. – This is pretty well

your relationship. Very often what happens is, no matter what I do to

help on the financial side, I actually can't

solve the problem because the problem

is between them. That's not your case. It's very clear that

you're very tight and you love each

other to death. When will you know

you have enough? Enough clothes, enough hats- – Honestly I probably

won't ever do that.

– $80,000 in consumer debt. Are you kidding me? – I know where

the money's going. – No you don't! Neither of you knew

where the money was going and I'm gonna show you

where the money's going. You don't know where

the money is going. (somber electronic music) There's your $80,000 in debt. You went off and

had an IVF treatment at an interest rate of 32%. These people are

stealing from you. If you can afford a baby, you should be able to pay

for your IVF straight up. – Yeah.

– Okay? 'Cause there's some planning

that goes into parenthood. And then you have all this

money on this credit card. At almost 20%. So you're not pro-actively

managing your credit, you're not figuring out how to

get your interest rates down. – No. – And your car loan Clint? At your payment, it'll take

100 months to pay it off, over eight years.

(melancholy guitar strumming) 'Cause you carry

forward negative equity. – Every time that we

trade in these vehicles, we lose money and

it just added up, added up onto his previous loan.

– Four cars in four years? Too many cars. What's that car

actually worth today? – Like $15,000.

– Okay. So that $15,000 car, you're gonna have to

drive for eight years and you're gonna

pay $51,000 for it. Ooh look, finally we got

something you understand. By the time it's all paid off, the way you're

doing it right now, you're $80,000 will have

cost you almost $145,000.00. – That's crazy. Yeah that kinda made me

step back and kinda look at what am I doing, why would

it be at that amount? – Okay so right now, you're housing is about $1,200, which is about 30%

of your income. And that's okay, you can spend up to 35%

of your income on housing.

But that's about to change. Clint, what's your new

mortgage payment gonna be? (somber jazz music) What's your property taxes? What are your

utilities gonna be? (Clint sputtering)

(Candice chuckling) What's the condo

gonna cost to insure? (Clint clearing throat) Maintenance and condo fees, you know what your

condo fees are gonna be? – Yeah, cheap. – Okay, so you actually

haven't got a clue. You just bought the

most expensive thing you're ever gonna buy

in your whole life. And he didn't even think to

check what it would cost? What is up with you? Every month you're overspending

by $2,755 every month. And if you keep it up, in five years you'll

be $677,000 in debt. (both chuckling)

(Gail snapping) – When he's silent it's 'cause

he's actually in trouble. – So my question is, is

that where you want to go? – No.

– You're sure? – Very sure.

– Very sure. – Okay, so will you do

anything I ask you to do? – Anything. – Over the next few weeks, I'm gonna give you a

series of challenges to do.

You do the challenges

to my satisfaction, I'll give you up to $5,000 to

help put a dent in this mess. If you don't do the

challenges to my satisfaction, you don't get the money. If you have the wrong attitude,

you don't get the money. – Okay

– We're gonna get your spending in line, okay? We're gonna put your debt

repayment on the front burner. And we're actually gonna try and get your guys

working together. You don't need

credit cards anymore, you can go get them

for me right now 'cause they're going bye bye. Coming up, challenge one leaves

Clint searching for words. – Get the hell outta here. – I am serious.

(couple laughing) ♪ Money money money

money money money money ♪ ♪ Money money money

money money money money ♪ (upbeat techno music) – Clint laughs off

his overspending. – I put the bills

underneath my pillow, wishing for the bill fairy.

(chuckling) – [Gail] But wife Candice

doesn't find it so funny. – I resent the fact that

he doesn't pick up on that we're in so much debt. – What does $80,000

worth of debt mean? How many cars is that? – One good one.

(Candice laughing) – I can see why

you have trouble.

With that debt,

they can't afford the medical assistance they

need to start a family. So the stakes are as

high as they can be. – He'll have all his stuff

but he won't have me. – [Gail] For the next month,

this couple will learn to live on a strict cash budget. No more credit cards. They'll complete

weekly challenges to tackle their money

and relationship issues and if they're

willing to change, I'll reward them with

thousands of dollars to pay down their debt. No changes, no money. You guys are

overspending by 75%. – (chuckling nervously) Oh man.

– So instead of the $4,000 a

month you have been spending, you will have only $1,000 to

spend on your variable expenses which is things like,

$100 a week for food. $100 a week for transportation. $25 a week for entertainment. Clothing and gifts? – Oh God it's

gonna be like zero. – Five dollars a week.

(Candice laughing) – Okay, oh God. – $17 dollars for other,

this includes your pet food. – Okay.

– Okay? Because your living on cash,

you have to write it down. Here's a budget binder. Make sure you track

every penny you spend. – Okay. – I feel that I'm

gonna have to step back and reevaluate things

that I feel are a need.

– It's time to hear about

your first challenge. You're actually spending

more on your transportation than on your housing. And that's because of that

silly little car go-around where you keep carrying the

debt from one car to another. So, since your car is all fire

and important to you buddy? You're gonna live in

your car for weekend. – What?

(Candice giggling) You're joking.

– I'm not. – Get the hell out of here!

– I am serious. – I love you!

(Candice giggling) – Because your car is the

most important thing to you- – Get the hell outta

here, are you serious? – I'm dead serious.

I mean, you're prepared to put your entire

financial situation at risk for the sake of a

car so, you know, you might end up having to

live in your car one day. So see what it feels like. – Yeah, that caught me

off guard completely. That wasn't even in my

spectrum whatsoever. – Part two is, you don't

know sweet diddly squat about the place you're buying. You need to know

what it's gonna cost for you two to

live in this place. So that you have a

budget that works. And you're gonna use his figures because your challenge this week is you're so hell-bent

on having a baby, you're job is to make a budget

that incorporates the fact that you wanna have a baby. So your costs are gonna go up, you have to figure all that out. Make it so, I'll

see you next week.

(upbeat funk music) (Candice knocking) – Yeah okay. To sleep in the car was

absolutely horrendous. I could not get comfortable. The thoughts I had last

night for the most part is pretty obvious, it's not

the smartest or brightest thing to spend more money on something

you spend a couple hours in than you know, keep a

roof over your head. – Hi I'm-

– With that in mind, Clint researches

the occupancy costs of their brand new condo and Candice adds up

the baby expenses. – Did you ever use formula

and what was the cost? – An average container, at

least $20, sometimes $30. – How many diapers- When I was doing

my IVF treatments, all I was thinking was of

the immediate you know, gratification of

becoming pregnant. – The day care costs are

obviously the one big thing. That's a huge thing

you have to consider, you look into beforehand. – I'm glad that she forced me to look at how much it

would cost to have a child. – Did you find out

about the condo? – Yeah, I was in

the dark for sure.

– Yeah.

– And the questions you asked me last week?

– Right. – I'd definitely

be landing them. – Okay good. And so, what was the

whole experience like, living in a car? – It gave me time to think

about what was going on and things like that-

– And what did you think when you thunk? – That I put us in, you know,

not the best of situations. – I thought for sure

that he would be like, F this, I ain't staying

in this (bleep) car. – Right, you were a good boy. – He was. – How did you find

doing the budgets? – I had to do a couple years

in order to get it to balance- (Gina laughing)

Yeah. Yeah it won't balance now. – When I did your budget I

couldn't get it to balance. – Okay. – You were several hundred

dollars over a month. You have a lot of debt and it's at a very

expensive interest rate. See all the stuff around here? These are all people

that needed money. So the first part of this week's challenge

gives you a choice.

Either, you sell $15,000

worth of your stuff to pay down the debt.

– Okay. – Or you find a way to

make an extra $700 a month. Somewhere generating that

on a consistent basis. – Between the two of us? – Between the two of

you to cover that. Part two is, to go to

a financial institution and say we need to do

a consolidation loan. And I need the lowest

possible interest rate. – Am I glad the bike's going? Hell yes!

(Candice chuckling) ♪ Money money money

money money money money ♪ ♪ Money money money

money money money money ♪ – You're actually

spending more on your cars than you're spending

on your housing. Clint has been facing

up to the reality of his financial situation. You're gonna live in

your car for a weekend. (Candice chuckling)

– What? – I thought for sure that

he would be like, F this! I was definitely proud of Clint. He did a complete 180 from

last week to this week.

– [Gail] That means

his wife Candice can start thinking

about the future. But with all that

expensive tech, I can't balance their budget. Candice and Clint had to

either come up with $15,000 by selling things or make an extra $700

a month between them. Their decision surprised me. – Clint and I decided to go with both option that she gave us. So we decided to sell my car. I know that taking the bus, it's gonna save

me a lot of money. Also I've spoken with my mom and I've decided to go

there and do my laundry. And I'm going to& be

her new cleaning lady and I've gotten a part

time job on Saturdays. It's just admin work

for a law office. (dirt bike revving)

(upbeat rock music) I was surprised that

Clint put up his bike but it's just sitting there

costing us money a month. – I love riding, it's

a nice escape but, I'll have time

for that later on. – I have visions of him

breaking his neck so, am I glad the bike is going? Hell yes!

(Candice chuckling) And Clint has two leads

for an extra part time job.

– For the time being, to help us get out of

our rut and you know, get things moving

forward a little bit. I can sacrifice some free time. – [Gail] And Clint found a way to turn another bad boy hobby into a source of income. – Tattooing, there's some more

things I could probably do. Get some business cards made

up, I don't know, flyers. I'm not scared of work at all. (jazzy pop music) – What'd you sell? – The car, my bike and yeah,

I got some employment leads. – Good. – And I got another

part time job- – Wow!

– With my old work, just on Saturdays.

– Okay well, you know what? If that's what it takes to

get you out of this hole, bust your butt now and then

you can have the life you want. Did you get the interest

rates on your loans down? – We went to a

different credit card, it's 5.99% for the

first two years. We're gonna roll

everything into it. Line of credit, credit card,

credit medical, all that. – So like, okay,

you did all of this? You put lots of thought into it.

So why didn't you do any

of this stuff before? – We needed somebody

to kick us in the ass. (both chuckling) – So, that's it,

that's all it took? – No, that's not all it took.

– No. – It's something that we'll

have to work on every day. – So are you ready for your

relationship rescue challenge? – Sure. – All I can tell you about

that is have a good breakfast. – Are you kidding me?

– That is (bleep) nasty. ♪ Money money money

money money money money ♪ ♪ Money money money

money money money money ♪ – [Gail] A few weeks ago,

Clint couldn't have cared less about his spending or his debt. – He sees it, he

wants it, he buys it. – [Gail] And his wife Candice had made poor

choices of her own. You went off and had a treatment

at an interest rate of 32%. But instead of making excuses,

Clint decided to man up. – I guess part of being an

adult is managing your finances. – Before I award them up to

$5,000 to pay down their debt, they have one last

challenge to complete.

(upbeat rock music) As they work through my

financial obstacle course, they'll have to stick

together for better or worse. – You made a commitment

to each other but your financial

irrepressibilities has put your future

on the ropes. Now one of you has to go

on the ropes for the other. Chose who does the

ropes challenge. Candice has stepped up. Yeah like that, keep your feet straight

like that in the middle. (Candice giggling) – The ropes were really,

really hard for me.

I wanted to stop

like a million times. I can't-

– Yes you can! – I feel like I'm gonna be sick! – You can, you're

good, you're good. – I think what kept

me going was Clint. – That's it, perfect! – In this challenge,

Candice can't work so Clint has to carry

the load all on his own. Crossing the creek caught me

off guard, it's very deceiving, you wouldn't think it

has that much power but it'll take you

out man, no problem. – [Gail] After two tough events,

it doesn't get any easier. – What the (bleep) is that? – The century egg. – Whoever sat out the ropes

course eats this challenge. – Thank God!

(Candice giggling) – [Gail] This Chinese delicacy

is made by curing an egg in a casing of mud and straw

for weeks or even months.

– The freaking thing is brown! – That is (bleep)

– Are you kidding me? – Nasty.

– Are you kidding? Should've done the ropes. Oh! (Candice gagging) (Clint coughing) I'm good, I can do it.

– Did you do it? I think it was great that

Clint ate that egg for me because if it was me, it

wouldn't have gotten done. – I think the biggest

lesson learned was, patience is important

to wait for something and not just go out and

grab it and forget about whatever consequences might be, whether there'll be enough

money for it or not. (gentle guitar music) – So that egg was

pretty gross wasn't it? – The egg was extremely gross. – But you did it. – I did it, yeah. – Proving yet again that

you're the man and you will do whatever it takes

to get the job done.

– Say it again.

(Candice giggling) – You are the man. – Thank you.

– You're welcome. What'd you learn this month? – I learned to

budget and I learned that Clint and I

can work together and when we work together

we can accomplish anything. – Candice learned a

lot, what did you learn? – Mainly being able to process

what is actually a need and what's a want. – [Gail] Not only have

they learned to prioritize but with a few simple

steps, Candice and Clint made a huge leap in

conquering their debt.

By consolidating most of

their remaining debt at 6% and paying it off in 20 months, they'll save themselves

over $56,000 in interest. When I got here, you were

overspending by $2,755 a month. You thought the kind of car

your drove was more important than just about everything else. And you couldn't work

together to save your lives. So that's all changed. How do you think you did

on a scale of one to five? – Four.

– A four? What do you think Candice? – I think a five! – You do, well you're right. – Oh thank you very-

– Hey, hey, hey! – Thank you.

(all laughing) – This made me realize that it

doesn't just work itself out you have to work hard at it and you have to

get a grip with it.

– I'm really, really happy

to see how well you did. I have for you also

a romantic getaway. – Thank you very much.

– Thank you so much! – You're very welcome. Now I'm getting my hugs.

– Thank you so much Gail. You've shown us a

brighter future. And now, he's gonna

be a perfect man! (Candice laughing) (upbeat rock music) ♪ Money money money

money money money money ♪ ♪ Money money money

money money money money ♪ ♪ Money money money

money money money money ♪ (machinery whirring)

(logo beeping)